Defining Net Operating Loss (NOL)

Net Operating Loss (NOL) occurs when a business’s allowable tax deductions exceed its taxable income in a tax period.

[ez-toc]

Net operating losses are significant because they allow companies to offset their future taxable income and potentially reduce their tax liability.

When a company experiences a net operating loss, it means that it has incurred losses during a specific period, which can be carried forward to offset taxable income in the future.

Net operating loss is subject to certain limitations, such as carryforward periods and restrictions on how much income they can offset in a given year. These limitations prevent abuse of the NOL provisions and ensure that companies do not excessively reduce their tax obligations.

Calculation and Example

Here’s a detailed explanation of each step involved in calculating Net Operating Loss (NOL):

Step 1: Determine the Eligibility of the Company

Before calculating the net operating loss, it’s important to ensure that the company meets the eligibility criteria set by the tax laws and regulations of the jurisdiction.

Generally, net operating loss deductions are available to businesses operating as corporations, estates, or sole proprietorships. However, the eligibility may vary based on the business’s legal structure and other factors.

For example, in cases of significant ownership changes, such as mergers or acquisitions, additional rules may apply to determine NOL eligibility and the utilization of NOLs.

Step 2: Check the Deductions

Calculate the allowable deductions for the specific period under consideration.

Deductions typically include various business expenses, such as operating expenses, salaries, rent, utilities, interest, depreciation, and amortization. These deductions are subtracted from the company’s total revenue or income to determine the taxable income.

Step 3: Calculate Net Operating Loss (NOL)

To calculate the net operating loss, subtract the total deductions from the taxable income.

The net operating loss represents the amount by which the company’s allowable deductions exceed its income, indicating a loss for the period.

Example:

Let’s say a company has a taxable income of $200,000 and allowable deductions of $300,000 for Year 1 with an applicable tax rate of 30%.

By subtracting the deductions from the income, we get $200,000 – $300,000 = -$100,000.

The company has a Net Operating Loss of $100,000 in this case.

In Year 2, the business turns a profit and records a taxable income of $250,000. Applying the tax rate of 30%, the tax liability would be:

$250,000 x 30% = $75,000.

However, since the business incurred a Net Operating Loss (NOL) in the previous year, it can use this loss to offset the current year’s taxable income. The business can deduct the NOL from its taxable income, reducing its tax liability to a huge extent.

To comply with tax regulations, retaining records for any tax year that generates a Net Operating Loss (NOL) is important. These records should be kept for at least three years after using the NOL for carryback or carryforward purposes or 3 years after the expiration of the carryforward period.

Eligible Deductions

To qualify for a Net Operating Loss (NOL), the loss should typically be from deductions from the following sources:

- Business losses include deductions from business activities reported on Schedules C and F (for sole proprietorships and farms) and losses from partnerships or S corporations reported on Schedule K-1.

- Casualty and theft losses: These deductions arise from events of casualty or theft due to a federally declared disaster.

- Rental property losses: Deductions from rental properties reported on Schedule E contribute to the overall net loss.

Certain rules restrict the deductions when calculating a Net Operating Loss (NOL). Generally, the following itemized deductions are not allowed for NOL calculation:

- Capital losses over and above capital gains.

- Section 1202 exclusion of gains from exchange or sale of qualified small business stock.

- Nonbusiness deductions exceeding nonbusiness income.

- The NOL deduction itself.

- Section 199A deduction for eligible business income.

- Personal exemptions.

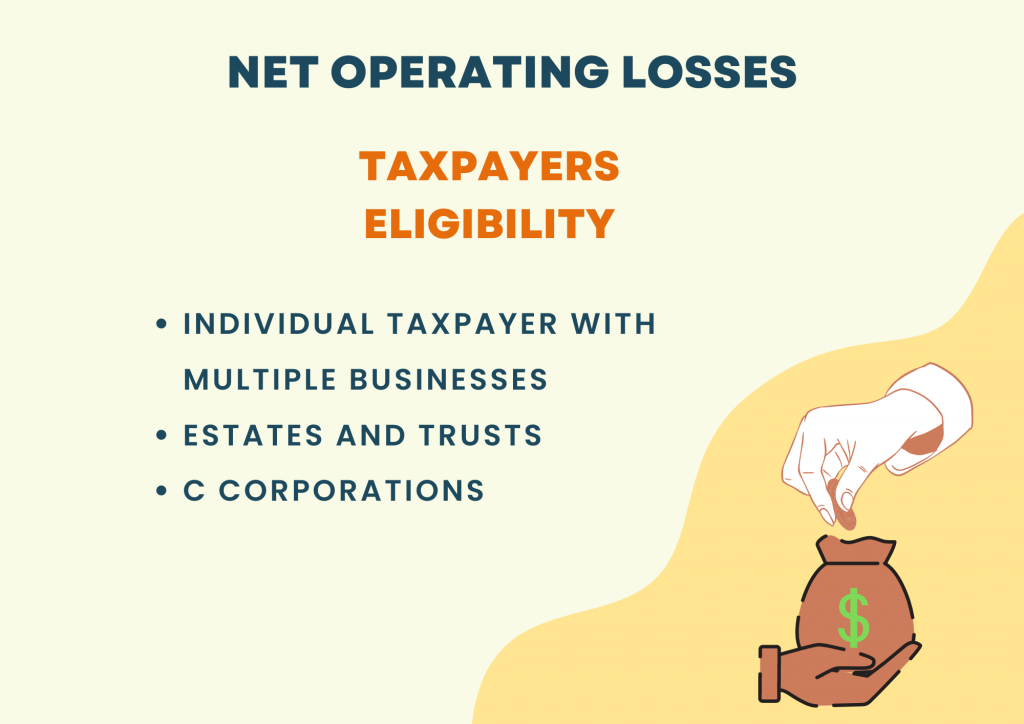

Taxpayer Eligibility for NOLS

Taxpayers who are eligible to deduct Net Operating Losses (NOLs) include:

Individuals

When an individual taxpayer has multiple businesses, the NOL deduction is calculated by considering the combined income and deductions from all businesses. The NOL can be deducted if it exceeds the income from other businesses conducted by the same taxpayer.

Estates and Trusts

Estates and trusts can deduct NOLs in a similar way to individual taxpayers. They can carry forward the NOL or back, adjusting the taxable amount for intervening years.

However, NOL deductions can only be passed on to beneficiaries in the year when the trust or estate ends with an unused NOL carryover.

Corporations

C corporations are allowed to deduct NOLs. C corporations recognize their gains and losses, and shareholders cannot claim the corporation’s NOLs on their tax returns.

But S corporations cannot deduct NOLs themselves; instead, shareholders of the S corporation can include their share of the NOL in their individual taxable income calculations.

Net Operating Loss Carryforward or Carryback

Net operating loss carryforward or carryback allows taxpayers to use their NOLs from one tax year to offset the taxable amount in other years. Net operating losses carryforwards refer to applying the NOL to future tax years, reducing taxable income, and potentially generating tax refunds.

Net operating loss carryback allows taxpayers to apply the NOL to previous tax years, seeking refunds for taxes paid in those years. A tax provision provides tax relief when a company incurs losses during a tax period. It aims to ease the tax burden for companies experiencing financial losses.

The choice between carryforward and carryback depends on the specific tax rules and regulations in place, and it can vary based on factors such as the taxpayer’s entity type and the applicable NOL tax laws.

Limitations

Starting from tax years after December 31, 2020, there is a limit on the NOL deduction.

- The deduction cannot be higher than the total NOLs carried from tax years before January 1, 2018.

- Additionally, the deduction is also limited to the lesser of two amounts:

- NOLs carried from tax years after December 31, 2017.

- 80% of the excess of taxable income (calculated without considering NOLs, Qualified Business Income, or section 250 deductions) over NOLs carried from tax years before January 1, 2018.

The NOL deduction has a maximum cap starting from 2021, which is based on the NOLs carried forward from previous years. It also considers the lesser of two factors: NOLs carried from recent years and 80% of the excess taxable income over NOLs carried from earlier years.

Net Operating Loss Vs. Net Income

| Net Operating Loss (NOL) | Net Income | |

| Definition | Net Operating Loss represents tax-deductible expenses exceeding taxable revenues | Net Income is excess of total revenues over total expenses |

| Tax Implications | Can be carried forward to compensate future taxable income and receive tax refunds | Subject to taxation |

| Financial Health | Indicates financial difficulty or losses | Reflects profitability and performance |

| Reporting | Negative figure on the income statement | Positive figure on the income statement |

Negative NOL for Small Businesses

Having a negative NOL can provide some benefits for small businesses. It allows them to reduce their liability in future profitable years by offsetting the income with the NOL amount. It can help the business recover from the loss and potentially lower its income tax burden.

By utilizing the NOLs effectively, small businesses can improve cash flow, reinvest in their operations, and position themselves for long-term success.

Small businesses must work closely with tax professionals to ensure compliance with the IRS (Internal Revenue Service) tax law and make informed decisions about using NOLs to maximize their financial benefits.

CARES Act and NOLs

The CARES (Coronavirus Aid, Relief, and Economic Security) Act, enacted in response to the COVID-19 pandemic, introduced significant changes to treating NOLs for businesses. One of the key provisions of the CARES Act related to NOLs was the temporary removal of the 80% taxable income limitation previously imposed under the Tax Cuts and Jobs Act (TCJA).

Under the CARES Act, businesses can carry back NOLs generated in tax years beginning 2018 to 2020 for up to five years. It means businesses can apply these NOLs to prior years’ taxable income and potentially receive refunds for taxes paid in those years.

The CARES Act allows businesses to fully offset their income with NOLs for tax years from 2018 to 2020. Businesses can use NOLs to reduce their liability to zero, providing immediate tax relief and potential cash flow benefits.

These temporary changes to NOL rules under the CARES Act provide businesses with increased flexibility and financial support during challenging economic times.

Impact of Changes in Tax Cuts and Jobs Act (TCJA)

The TCJA presented many changes that impact NOLs. For example, before the TCJA, net operating losses and carried forward 20 years and could be carried back two years.

However, the TCJA eliminated the carryback provision for most taxpayers, allowing only a carryforward option. Additionally, the TCJA limited the NOL deduction to 80% of taxable income for losses incurred in tax years after December 31, 2017.

These changes have implications for businesses with net operating losses. The elimination of the carryback provision means that net operating losses can exclusively be used to offset future income. The limitation of 80% of taxable income reduces the immediate tax benefit of net operating losses, as businesses can only offset a portion of their income.

Businesses need to understand these changes and plan accordingly. While the TCJA provides some limitations on NOL utilization, it also offers opportunities for strategic tax planning.

The TCJA raised the Alternative Minimum Tax (AMT) exemption amounts, reducing the number of individuals subject to this parallel tax system. It relieved the burden for taxpayers who previously had to calculate their tax liability under the alternative minimum tax and the regular tax system.

Consulting with tax professionals can help businesses navigate the complexities and optimize their tax positions in light of these changes.

Way Forward

Net operating losses offer businesses a valuable means to navigate tax liabilities and recover from financial setbacks. With recent changes in tax laws, including the TCJA and the CARES Act, understanding the evolving IRS (Internal Revenue Service) regulations surrounding net operating losses is essential.

Businesses can optimize their tax strategies, safeguard their financial health, and seize growth opportunities by effectively managing net operating losses and staying informed about updates. Head to the Akounto blog for more such articles on various accounting concepts.