Operating income (operating profit) is derived from core activities of the company, while net income includes operating and non operating income.

Core business activities includes primary revenue streams from the activities for which the business is incorporated, thereby contributing towards operating income.

What’s covered in the article

Non operating income refers to all the other sources of income like royalties, patent income, franchisee payments, etc. which are additional income streams, other than primary business income.

Both operating and net income are salient metrics in preparing the income statement.

When it comes to operating income vs net income, the primary differentiator is the non operating income which is excluded to calculate operating income.

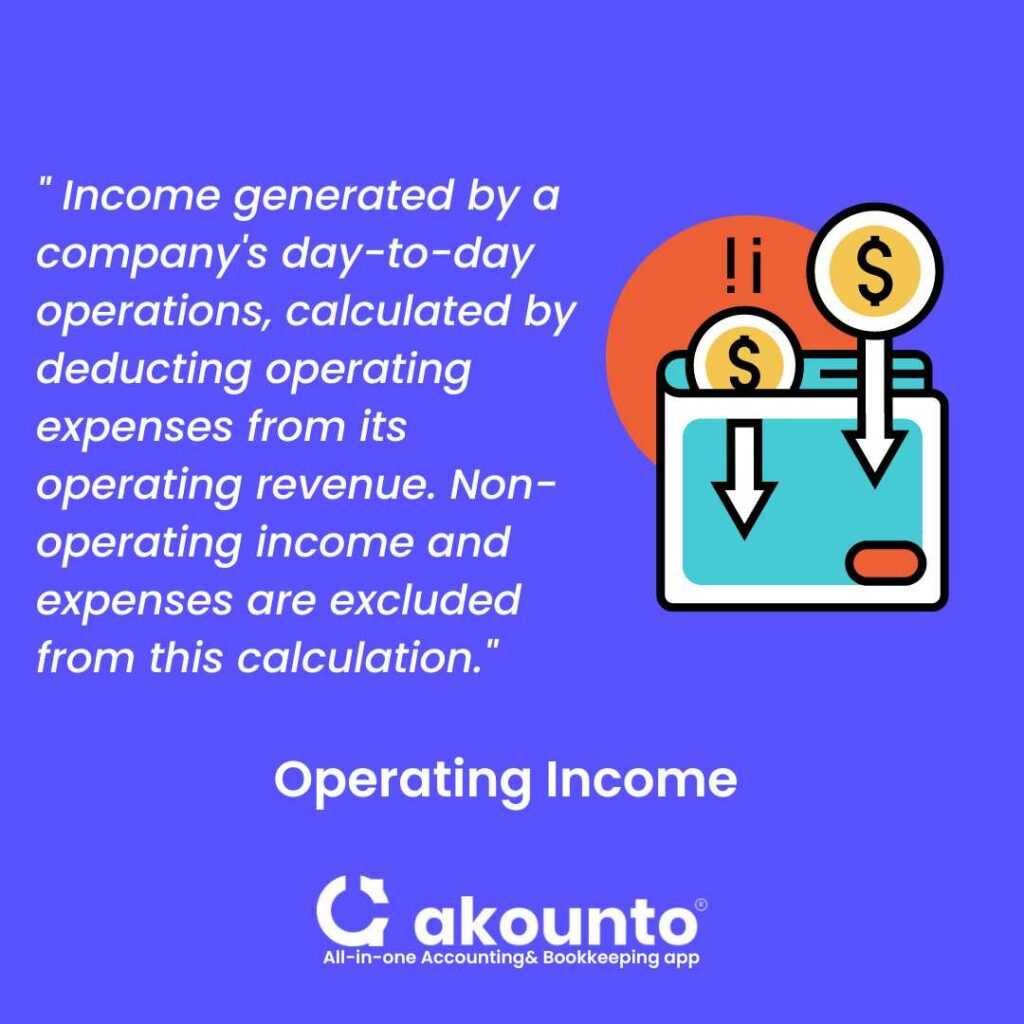

What is Operating Income?

Operating income refers to the income from the day-to-day operations of a business. Operating income is computed by subtracting operating expenses from the company’s operating revenue. It, however, doesn’t include non-operating income and expenses.

One-time expenses and one-time income are not considered in the computation of the operating income as they don’t form a part of the daily operations of a company.

Positive operating income is termed as operating profit, that is favorable when the company can generate profits after covering non-operating and general expenses. It is a tool to measure the operational efficiency of the company

Analysts or investors use operating profit as a criterion to examine the ability of a company to generate profit and recover non-operating expenses. Operating profit is also known as operating income.

Formula for Computation of Operating Income (operating profit)

Operating income can be computed using various formulae which are given as follows:

Operating income (operating profit) = Total Revenue – Direct Costs – Indirect Costs

Operating income (operating profit) = Gross Profit – Operating Expenses – Depreciation – Amortization

Operating income (operating profit) = Net Earnings + Interest Expense + Taxes

Operating income (operating profit) = Total revenue – Cost of goods sold – operating expenses – depreciation and amortization

Components of the formula

Component 1: Total revenue refers to the total income from the sale of the goods and services

Component 2: Cost of goods sold indicates the cost directly associated with producing the goods.

Component 3: Operating expenses of a company refer to the cost of running day-to-day operations.

Example: Rent, wages and salaries, Insurance, Repairs & maintenance, etc.

Component 4: Depreciation refers to the loss of value of a tangible fixed asset over time. Amortization refers to the falling value of intangible assets over time.

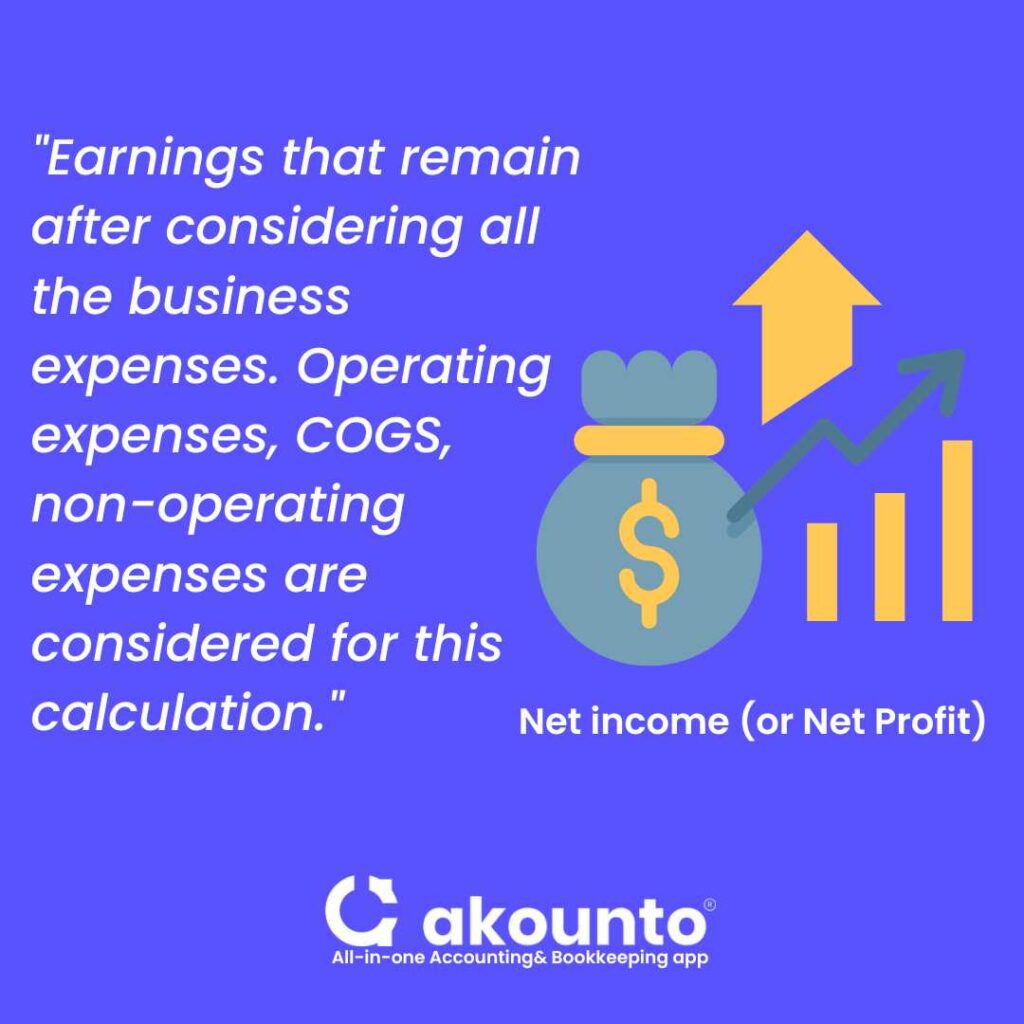

What is Net Income?

A company’s net income refers to the earnings that remain after considering all the business expenses. It indicates that in addition to the operating expenses and cost of goods sold, non-operating expenses such as taxes, interest expense on outstanding debt, extraordinary income and expenses, etc., are also considered. Net income is also known as net profit.

Net income is considered the bottom line as it is the last item in the income statement. The bottom line signifies effective management through cost savings and revenue generation. Net income is synonymous with net earnings and earnings after tax. It is the basis for computing earnings per share.

Earnings per share of a company is an important measure to determine the return on the stock on a per-share basis. It helps the investors in decision-making because

It highlights the profitability of a business

It assures the returns on their investment

It emphasizes the worth of the share in the market

Further, net income is also vital in determining return on assets, return on equity, and various other ratios that prove a business to be creditworthy.

Formula for Computation of Net Income

Net income = Total revenue – Total expenses

Net income = Operating income + Extraordinary income – Non-operating expenses – Interest expenses – Taxes – Extraordinary expenses

Components of the formula:

Component 1: Operating income refers to the revenue from the core operating activities of the company.

Component 2: Extraordinary income refers to gain from unusual or infrequent events. They are considered additional income streams since they are not generated from normal business activities.

Example: sale of an asset

Component 3: Extraordinary expense refers to loss from unusual or infrequent events.

Example: lawsuit

Component 4: Non-operating expenses are those not related to the core operating activities of the company.

Examples: Legal fees, Overhead expenses such as general, selling, and administrative expenses, Vehicle expenses, Office utilities, Research expenses, Accounting expenses, etc.

Numeric Example of Net income

P & G Inc. earned total sales worth $ 20,000 in FY-2022. Other details in the income statement are as follows: (Amount in $)

Cost of goods sold: 12,000

Rent expense: 500

Wages: 1,000

Depreciation: 200

Interest income earned: 100

Selling expenses: 875

Accounting expense: 1500

Sale of asset: 80

Interest expense: 130

Research expenses: 100

No. of shares outstanding: 1000 shares

Calculate net income and operating income based on the above information.

Solution:

| Particulars | Computation | Amount ($) |

| Revenue | 20,000 | |

| Less: Cost of goods sold | (12,000) | |

| Gross income | 8,000 | |

| Less: Operating expenses Rent Wages | 500 1,000 | (1500) |

| Less: Depreciation | (200) | |

| Operating Income | 6,300 | |

| Add: Interest income | 100 | |

| Add:Extraordinary income (Sale of asset) | 80 | |

| Less: Interest expense | (130) | |

| Less: Operating expense Accounting expense Selling expense Research expense | 1,500 875 100 | (2,475) |

| Net income or net profit | 3,875 | |

| No. of shares outstanding | 1,000 | |

| Earnings per share (Net income/ No of shares outstanding) | 3.875/ share |

From the above, information we can also arrive at operating profit margin.

Operating margin = operating income/ Total sales = 6300/20000 * 100= 31.5 %

Key Differences between Operating Income and Net Income

| Basis of difference | Operating income | Net income |

| Meaning | Operating income is the income after deducting operating expenses. It is the income from the core activities of the business. | Net income is the income remaining after deducting non-operating expenses and other one-off items. |

| Formula | Operating income = Total revenue – Cost of goods sold – operating expenses – depreciation and amortization | Net income = Operating income + Extraordinary income – Non-operating expenses – Interest expenses – Taxes – Extraordinary expenses |

| Uses | Used to compute return on capital employed | Used to calculate the company’s earnings per share, return on investment, return on assets, etc. |

| Importance | Operating income shows the proportion of revenue that gets converted into profits. | Net income emphasizes the earning potential of the business. |

Conclusion

In the discussion of operating income vs net income, the choice of metrics depends upon the analysis. Operating income that results in operating profit depicts the efficiency of business activities only, excluding other non primary sources of revenue.

The net income on the other hand shows organization wide efficiency.

The computation of operating and net income helps investors determine the company’s profitability resulting in better decision-making in a company.

All-in-one accounting software, Akounto, assists small businesses in maintaining accounting records and generating useful financial reports. To know more, visit our website.