Escrow is an arrangement in which a trusted, neutral third party holds assets, funds, documents, or money while the buyer and seller complete the transaction.

The trusted third party is called an “escrow agent.” The escrow agent can be an individual, bank, non-banking financial institution, or a company.

An escrow agreement defines the roles and responsibilities of the buyer, seller, and escrow agent. It also outlines the obligations or conditions of the transaction that must be fulfilled so that the escrow agent can transfer the consideration (assets, funds, documents, etc.) to the other party.

An escrow agreement can be made for any legal transaction. The money or consideration to be exchanged is kept in the custody of the escrow agent, and when the buyer and seller fulfill their obligations, the escrow agent transfers the “consideration” to the buyer. The escrow agent charges a fee for their services.

The term “in escrow” refers to when the asset under consideration is held by an escrow agent, a third party who acts as a custodian while the buyer and seller fulfill their contractual obligations. The term is commonly used in real estate transactions.

Escrow protects buyer and seller in a legal transaction and is, therefore, considered a good option, especially in mortgage agreements.

In corporate accounting, when sale proceeds are held in an escrow account for any claims or inspections, then as per the revenue recognition principle, the revenue will only be recognized when the funds are released to the seller.

Need for Escrow Accounts

Escrow minimizes the risk of financial fraud by acting as a trusted and neutral intermediary that provides a secure way to handle high-value transactions. The risk can be of either deliberate fraud or any misrepresentation.

As an intermediary, the escrow agent releases the assets or money when both parties (buyer and seller) are satisfied with the performance of the agreement, thereby providing the safety of the transaction.

Escrow-based transactions can be legally mandated, as in some jurisdictions, they are required in the cases of mergers and acquisitions, mortgage agreements, auctions, gambling, B2B commerce, contingency agreements, etc.

Escrow companies provide escrow services for complex, large, and high-value transactions. The risk-factor is covered for both buyer and seller. The escrow service provider acts as an intermediary and facilitates the transaction, thereby bridging the trust between unknown and unrelated parties.

In the USA, escrow services are largely used in mortgage arrangements, especially to secure the payment of property taxes and insurance premiums during the term of the mortgage. Nowadays, escrow is also being done for transactions related to the sale or purchase of cryptocurrency, websites, commercial property, etc. With the advent of cost-effective escrow services, the buyer and seller are adopting escrow whenever there is a lack of trust or the parties are unknown to each other, like in the case of auctions.

Working of Escrow

The escrow agreement lays down the conditions or terms which must be fulfilled so that the transaction is successful. These conditions are mentioned in the escrow agreement. This agreement, along with the asset, is held by the escrow agent. When the transaction is complete, then the escrow agent will scrutinize (“escroue” in French) the transaction and, upon finding that the conditions are met, will only then disburse the escrow property. If the conditions are not fulfilled, then the amounts will be returned to their respective owners.

Thus, we see that there is an escrow agreement between the buyer and the seller, which states the following:

- Purchase price

- Defining the scope of the transaction

- Identifying the asset/ commodity to be exchanged for the money (purchase price)

- Terms and conditions of the transaction

- Expected timeline within which the transaction is to be completed.

- The preference of escrow service providers.

After the escrow agreement, the contracting parties select or approach the escrow service provider, generally a bank, a financial institution, or a licensed escrow service provider, to act as an escrow agent and hold the asset (property, IPR, actioned item, website, other digital assets, artifacts, etc.) from the seller’s side and the money (purchase price) from the buyer’s side.

Now, the buyer has time to check the seller’s claims and can conduct an inspection or due diligence. In case there are any repairs, updates, etc., the buyer can ask the seller to perform them. If the seller refuses, then the buyer can tell the escrow agent that he is not satisfied with the transaction, and the amount and asset will be returned to the respective owners, and the transaction will be canceled.

The buyer can verify the items, claims, documentation, etc. Both buyer and seller can have their own set of obligations. The seller may want to check if the buyer is the genuine party before transferring ownership or the delivery of goods. Any condition that is contingent on the seller can be fulfilled if it is mentioned in the escrow agreement.

The escrow agent checks, verifies, or scrutinizes the transaction as per the agreement. Once all the conditions mentioned in the agreement are met, ownership is transferred to the buyer, funds are released to the seller, and the transaction is considered complete.

The escrow agent will provide the documentation to the contracting parties after the closing as evidence of the transaction and the conditions that were successfully met.

Types of Escrow Accounts

Real Estate Escrow

The buyer deposits the amount (purchase price) in the escrow account held by the escrow agent. This gives the seller surety that the buyer is genuine and has the appropriate funds to purchase the property. On the other hand, the buyer can now conduct due diligence on the property, i.e., whether the title is clear, whether there is any lien against the property, whether there are any damages to the property that may require repairs, etc.

Once the buyer deposits the purchase price in the escrow account, the seller will have to withdraw the property from the listing because by submitting the amount, the buyer has proved his seriousness about purchasing the property and initiated the transaction process. The buyer can now ask the seller for verification and any repairs if needed, which are called the escrow instructions. The scope of escrow instructions will be mentioned in the escrow agreement.

If the seller fulfills the obligations of the agreement, the escrow agent will transfer the amount to the seller, and the ownership title will be transferred to the buyer. If the escrow agent finds that the conditions of the transaction are not met, the transaction will be canceled, and the amount will be returned to the buyer. Usually, the escrow service provider charges 1-3% of the transaction value as the fee for escrow services.

Mortgage Escrow

Mortgage escrow ensures the timely payment of property taxes, mortgage insurance premiums, homeowners insurance premiums, etc. The mortgage escrow account continues with the tenure of the mortgage loan. It is opened separately, and the homebuyer deposits a monthly, bi-annually, or quarterly amount for the payment of loan, interest, taxes, and insurance premiums.

The mortgage lender will use this amount to ensure timely payments of taxes and insurance. The payment will be automatically made by the mortgage lender, and the homebuyer will not need to do anything else. An additional “cushion amount” is also added to the regular mortgage payment.

Escrow is Judicial Cases

In court cases, suits, or settlements in class actions, the court may ask the defendant to deposit the total amount into a court-administered escrow account. In case of a remediation, mitigation, or settlement, the court can distribute the money to the plaintiffs or use the amount as per the court’s decree. The defendant, once deposited in the escrow account, is not further responsible for the disbursement of the money.

Internet Escrow

Similar to traditional escrow, internet escrow requires the money to be deposited to the escrow service provider (escrow agent). The aim here is to protect the buyer and seller from any fraud, misrepresentation, mistake, etc., and give enough time for due diligence and further scrutiny by the escrow agent. Internet escrow companies in California (USA) are licensed by the California Department of Business Oversight. The escrow company licensing started in California on July 1, 2001. The first licensed escrow company was established in 1999 by Fidelity National Financial.

Example of Escrow Account

The following example gives the scenario of a typical real estate escrow:

Stage 1: Pollyanna wants to buy a house from Ashley. They both decide on a purchase price of $250,000 and frame a purchase agreement that contains terms and conditions regarding the inspections, repairs, timing of the whole deal, manner of payment, ways to verify title, zoning, lien, etc., and any other clause related to mandatory disclosure by Ashley.

Stage 2: Pollyanna and Ashley decide to avail of escrow services and look for a licensed escrow company to act as escrow agents. They both shortlist a company in their state, and Pollyanna deposits earnest money into the escrow account, which is around 1-3% of the total purchase price. This deposit is to show the genuineness and commitment of the buyer to purchase the property. On the deposition of the earnest money, Ashely has to withdraw the property from the listing and cannot make a sale offer to any other person.

Stage 3: The escrow agreement states that the time of escrow is 30 days and can be extended by 30 days if needed. This gives Pollyanna to inspect the property and raise any matter of repairs. Pollyanna can also hire a legal firm to verify the title of the property and any pending issues. This process is to vet the property. The contingency clause in the contract requires Ahsley to conduct repairs before selling the property.

Stage 4: Ashley has to provide Pollyanna with title documents, a deed, proof of financing, and insurance for the escrow company.

Stage 5: If Pollyanna needs to secure the funding, the lender will also deposit the amount in the escrow account.

Stage 6: The escrow company will also verify title search, and ensure no encumbrances on the property or pending liens. On satisfying these requirements and the requirements by Pollyanna, the escrow company will transfer the ownership title to Pollyanna and the amount to Ashley.

Stage 7: All the concerned parties will decide on a date to conclude the transaction. Upon completion of the final paperwork, the funds will be disbursed. It is the responsibility of the escrow company to ensure that the closing costs are settled and both parties get their dues.

Stage 8: The escrow company will register the sale deed with the government authority, usually at the county’s recorder’s office, and will furnish the final documents to Ashley and Pollyanna.

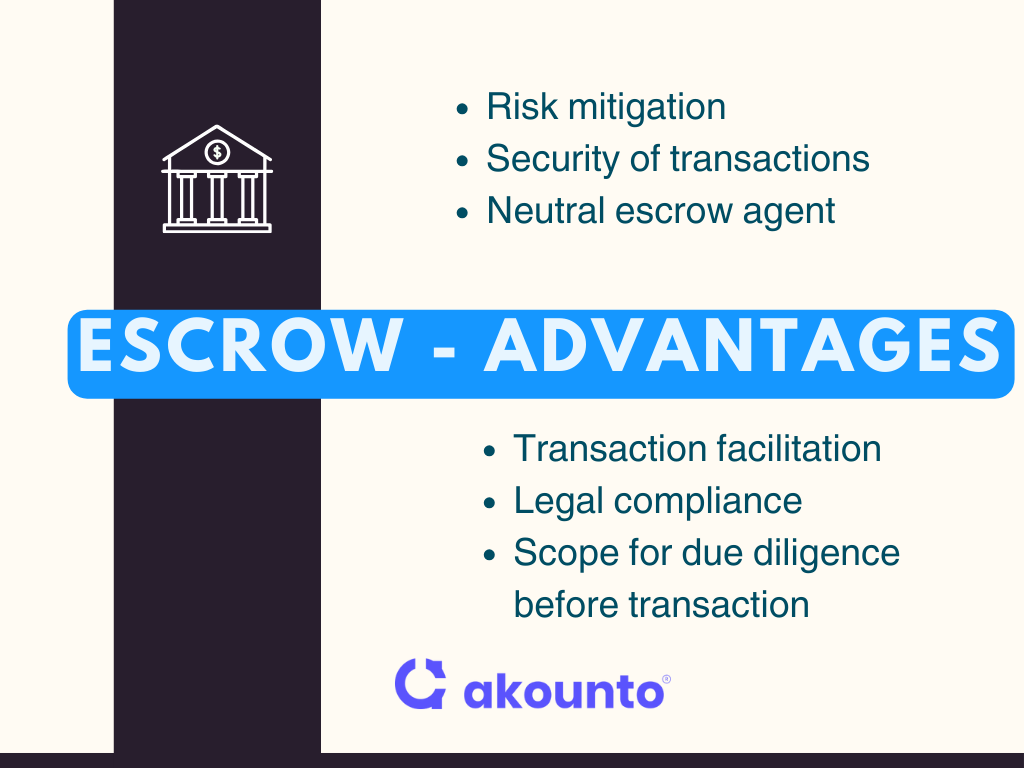

Pros and Cons of Escrow Account

Pros

- Security of transactions as escrow reduces the risk of fraud, misrepresentation, mistake, oversight, or non-payment. It gives the buyer the time for due diligence and verification of the seller’s claim and to scrutinize the title etc.

- Risk mitigation for buyer and seller. Escrow services easily establish the trust and authenticity of transactions between unrelated parties who are unknown to each other. Once the buyer deposits the amount (or token amount) in the escrow account, it proves the authenticity of the buyer, and the seller is assured of the payment. Similarly, the payment is not transferred to the seller until the conditions stated in the escrow agreement are met.

- The impartiality of the escrow agent ensures that the service provider will act in accordance with the escrow agreement and not in favor of any party.

- The escrow agent or service provider facilitates the transaction and transfers the funds and ownership of the assets once the conditions are fulfilled.

- The escrow arrangement may be required as a legal or regulatory requirement.

Cons

- The overall transaction amount is increased as the escrow service providers normally charge a fee as a percentage of the total transaction. The fee normally lies within the range of 1 to 3%, but it can go higher depending on the complexity of the transaction.

- In case of any disputes, the escrow agent may require certain due diligence, which may delay the transaction.

- When the funds are deposited with the escrow company, the buyer has no control over the funds, and the funds are locked until the transaction is over. Thus, the buyer loses control of his finances even before the transaction is complete.

- Escrow is not applicable or suitable for small transactions.

- The complexity of escrow and making agreements can keep parties away from taking escrow services.

How long can money be held in escrow?

In real estate transactions, the escrow amount can be held for 30 to 60 days, while a normal escrow is usually around 30 days.

This gives ample time for the parties to verify. An escrow can be closed in at least 10 days.

Use Cases of Escrow

- In underwriting, while offering securities like bonds or stocks, the underwriters can demand the initial subscription amount be deposited in an escrow account to meet regulatory requirements or cover specific expenses. These funds can either be released to the issuer or added to the purchase price of the bonds or stocks issued upon completion of any compliance.

- In venture financing, the angel investor may place the finding issued to the startup or a small business in an escrow account. The funds can be released subject to meeting the business milestones.

- In mergers and acquisitions, which are handled by investment banks, a portion of the purchase price is deposited into the escrow account. If offers risk mitigation to the buyer in the form of recourse if the seller violates or breaches any condition or warranties in the post-closing phase. In such a scenario, the escrow amount is used to cover indemnification charges.

Conclusion

If you are buying or selling a property, business, or any high-value asset and are not aware of the bonafide of the other party, then opting for escrow services will protect you from any fraud and any act of omission or commission that can lead to your financial loss. In such a scenario, bearing 1-3% of the escrow fee is much cheaper than bearing total loss. Doing business is always riddled with risks, and as an entrepreneur, you must be prepared to mitigate the risks by having requisite knowledge of business tools, services, and financial concepts.

Visit Akounto Blogs for more information, that is helpful for you to run your business smoothly and securely.