Bookkeeping is vital for businesses as it aims to keep a complete and accurate record of all the financial transactions in a systematic orderly, logical manner. It provides financial information to both internal and external users, which will be beneficial for sustainable growth and informed decision-making.

Effective Bookkeeping eventually ascertains the final accounts of the company, namely the Profit and Loss Account and the Balance Sheet. It ensures that businesses stay up to date with their financial transactions & assess where the business is heading.

As soon as your business grow, Bookkeeping helps business leaders make strategic decisions & change their business plans to unlock new levels of revenue & income. It involves aspects such as how much money your business owes and receives, what is the investment amount and the profit derived from it and much more.

From tracking revenue and expenses to managing cash flow and preparing for tax obligations, the role of Bookkeeping is vital for every business owner and stakeholder. It allows you to easily retrieve crucial financial information and save businesses from the stress of searching for documents during deadlines.

Regular Bookkeeping ensures that businesses stay compliant, avoiding any penalties or legal issues. This article will delve into why Bookkeeping is important and how it can benefit your business. Not everyone is an expert when it comes to doing the books for their own company, but it’s easier than you think to get started and keep going.

Bookkeeping vs Accounting

Though, Bookkeeping and Accounting both are used for financial planning and management. Bookkeeping is all about maintaining financial records in an organized manner while Accounting is process where the accountant need to adjust the entries, analyze the data & prepare comprehensive financial reports & statements.

Bookkeeping focuses on day-to-day financial activities and involves tasks such as maintaining ledgers, recording transactions, and reconciling accounts to ensure accuracy and transparency in financial records. On the other hand, accounting plays a more analytical and strategic role, interpreting financial information for decision-making.

Bookkeeping, also known as “Outsourced accounting”, refers to organize and record every financial detail where payment occurs to avoid inconsistencies or discrepancies. Accounting helps in determining the financial health of a firm and conveys the credibility of a company to the market.

Bookkeeping focuses on capturing the raw financial data, accounting elevates this data into actionable insights through financial analysis, budgeting, and strategic planning. The purpose of accounting is to provide a clear view of financial statements to its users, which includes investors, creditors, employees, and government compliance.

Thus, Bookkeeping deals with identifying and recording financial transactions only whereas accounting refers to the process of summarizing, interpreting, data analyzing and creating deeper insights for the financial position of a business.

Single Entry vs Double Entry Bookkeeping: What’s Best for Your Business?

Single entry Bookkeeping is best for small businesses with few transactions. It involves recording transactions only once in a cash book or Journal, either as an income or an expense. This method can be used to maintain a simple checkbook and keeping a daily or weekly record of your cash flow. However, it does not track assets and liabilities, making it less comprehensive as compared to double-entry Bookkeeping. It doesn’t allow accurate due diligence of your financial transactions.

The single-entry system of accounting reflects the current balance in your books but doesn’t categorize the transactions into expenses, fixed assets, or advances. You will have to pass a different entry of all these transactions to provide accurate financial reporting.

Double-entry Bookkeeping, on the other hand, is the gold standard for accurate financial records. It records every transaction twice- once as a credit and once as a debit, ensuring that the accounting equation (Assets = Liabilities + Equity) remains balanced. Here, every debit entry in an account should be equal to the corresponding credit entry in another account. This method provides a more accurate and comprehensive view of your company’s financial health, helping you to make smarter business decisions.

How to get started with Bookkeeping?

Starting Bookkeeping for your business involves recording, organizing, and analyzing your company’s financial transactions. Let’s discuss the process for better understanding.

- Recording Accounting Transactions: The process begins with recording all your financial transactions, including sales, purchases, expenses, and payments. Each transaction is meticulously documented to maintain financial records.

- Classification and Categorization: Once recorded, transactions will be classified and categorized based on their nature and purpose. This step ensures that financial information is properly organized and easily accessible for analysis and reporting.

- Posting to Ledger: The recorded transactions are then posted to the most appropriate ledger accounts, such as accounts receivable, accounts payable, cash, and inventory. This step involves a clear and concise view of your every transaction, enabling small business owners to track their financial position effectively.

- Trial Balance: A trial balance is periodically prepared to ensure that debits are equal to credits, thereby validating the accuracy of the recorded transactions. Any discrepancies are identified and rectified instantly to maintain the integrity of such financial reports.

- Financial Statement Preparation: Based on the ledger accounts and trial balance, financial statements such as the income statement and balance sheet are prepared. These statements offer deep insights into a company’s financial performance, profitability, and liquidity.

- Analysis and Reporting: Finally, the prepared financial statements are analyzed for better business performance, cash flow management, and financial health. This analysis helps business owners in making informed decisions and strategizing for future growth and success.

Basic Books of Accounts

The type of Books that a business retains depends on many factors, such as business size and financial capacity. From recording transactions in the Journal to posting them in the ledger and managing petty cash, each component plays a vital role in the bookkeeping process, contributing to the overall financial health and success of the business. Here are the basic Books of accounts that every taxpayer like. Let’s take a look:

Journal

Bookkeeping important for small businesses because of original entry book and the Journal serves as the first point of entry for all financial transactions. Each transaction is recorded chronologically in the Journal, along with the details such as the date, description, and amount using the principle of “debit and credit”.

Ledger

Once transactions are recorded in the Journal, they are subsequently posted to the ledger. The ledger is referred to as the final entry, which serves as a collection of individual accounts organized financial records, each representing a specific asset, liability, equity, revenue, or expense. Transactions are categorized and posted to the appropriate ledger accounts, providing a detailed record of each account’s entries to get the reconciled balances. Through the ledger, business owners can track their Assets, Liabilities, Owner’s capital, Revenues, and Expenses.

Petty Cash

Petty cash represents a small fund maintained by businesses to cover minor expenses such as office supplies, stationery, meals, client lunch, stamps, etc. The petty cash book serves as a record of these disbursements, documenting each expenditure along with the purpose and amount. Petty cash provides greater flexibility when compared to demand drafts or bank cheques. For instance, a huge organization with hundreds of employees will have a petty cash fund for each department.

Day Books

Day Books, also known as subsidiary books or special journals, are used to record transactions that are similar in nature. In big business institutions, it is not easy to record all the transactions in one Journal and post them into various accounts. So, for the easy and accurate recording of all the transactions, the Journal is subdivided into many subsidiary books, which are as follows:

- Cash Book

- Purchase Book

- Sales Book

- Purchase Return Book

- Sales Return Book

- Bills Receivable Book

- Bills Payable Books

- Journal Proper

These day books streamline the recording process for recurring transactions, ensuring efficiency and accuracy in financial record-keeping.

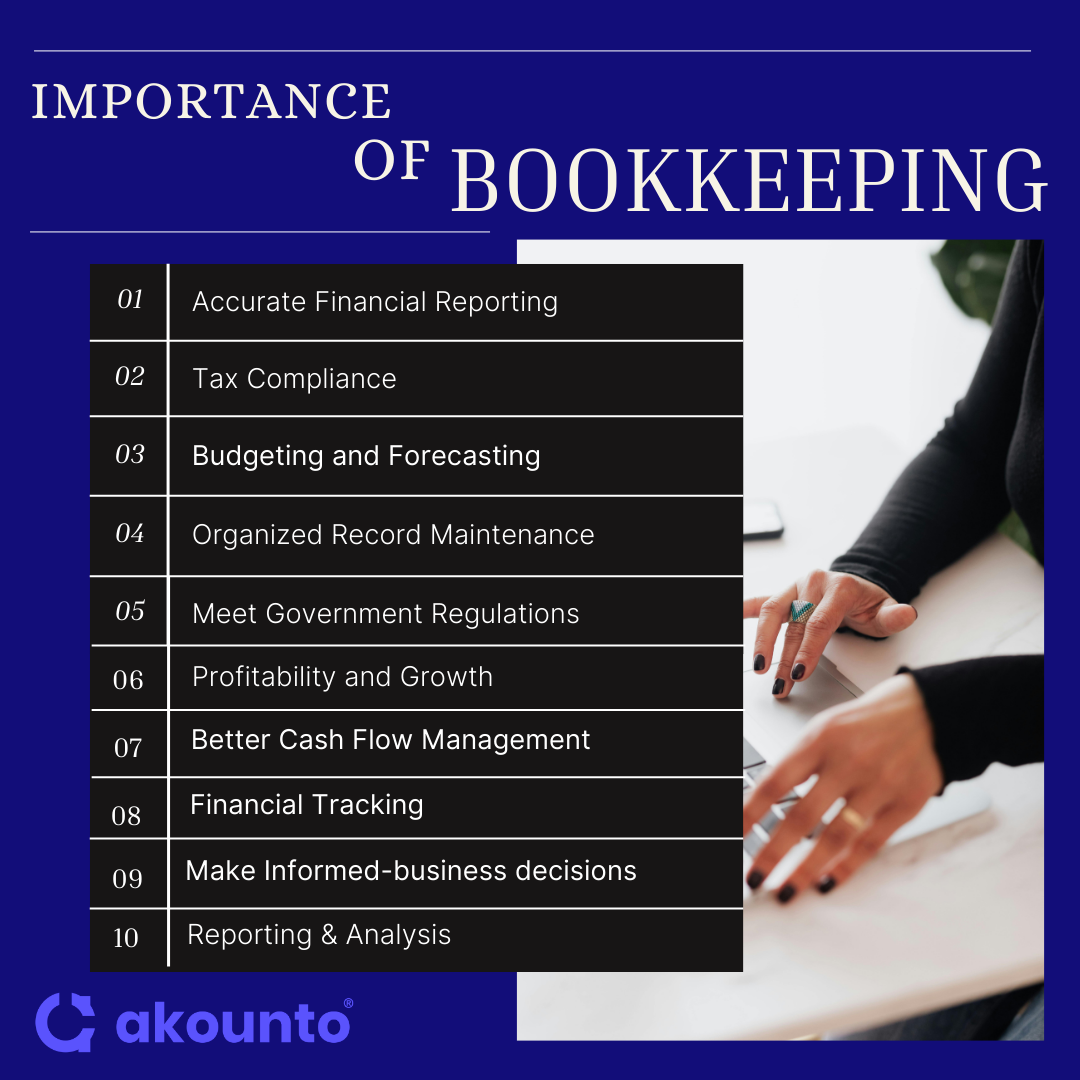

Importance of Bookkeeping

Bookkeeping plays a lead role in how an organization operates. When a business is up and running, spending extra time and money on maintaining proper records is crucial for its smooth functioning. With the help of Bookkeeping, business owners can analyze the financial health of their venture, make fully informed decisions, keep their business financially stable, and pay taxes on time.

By having an accurate and comprehensive overview of their finances, they can even ensure the development and prosperity of their companies. There are a variety of reasons why Bookkeeping is important and how it helps to grow your business ecosystem.

Accurate Financial Reporting

Maintain accurate financial records is a crucial part of Bookkeeping. It can provide businesses with valuable insights into their current financial situation. With Bookkeeping, businesses can create financial statements that reflect their financial position, enabling them to make informed-decisions.

Financial management bookkeeping enables business owners to track income, expenses, assets, and liabilities effectively, providing a clear snapshot of their financial position at any given time. Financial reporting can help businesses by evaluating profitability, assessing liquidity, identifying cost-saving areas, recording and organizing financial transactions, and recognizing potential investment opportunities.

Tax Compliance

Another important aspect of proper Bookkeeping is meeting tax compliance standards set by the Internal Revenue Service (IRS) and preparing accurate tax documentation. By diligently recording income, expenses, deductions, and credits throughout the year, small business owners can streamline the tax preparation process and minimize the risk of errors or discrepancies. These can include underpayment or over-payment of taxes, which can result in hefty fines or a possible audit.

Budgeting and Forecasting

Accurate Bookkeeping is crucial for budgeting and forecasting purposes, allowing businesses to allocate financial resources effectively and plan for future expenses. By analyzing financial statements, businesses can gain valuable business insights. They allow them to identify cost-reduction or where to invest resources to reach their long-term financial objectives.

For instance, analyzing financial statements can assist businesses in predicting their cash flow and planning for upcoming expenses. This enables them to manage cash flow, control costs, prioritize investments, and make wise decisions about their future financial needs.

Organized Record Maintenance

Bookkeeping helps business owners organize their financial records. This ultimately simplifies the process of filing financial statements, tax returns, financial audits, etc. When it comes time to budget, apply for loans or grants, or see if you’re turning a profit, Bookkeeping allows you to find the information you need quickly.

Basic accounting for small business lets you organize your information in one place and help you plan out bill payments. By seeing when your bills are due, you can organize expenses on your calendar.

Meet Government Regulations

Bookkeeping is essential for businesses to comply with governmental regulations, such as those of the Securities and Exchange Commission (SEC) or the Financial Industry Regulatory Authority (FINRA).

Failure to adhere to these guidelines may result in hefty fines, legal repercussions, or even the loss of licenses. Most recently, it’s the Making Tax Digital (MTD) initiative with which the government is expecting businesses to comply.

From filing income tax returns to complying with sales tax regulations and payroll tax obligations, maintaining business records is crucial for meeting regulatory requirements and avoiding costly penalties.

Profitability and Growth

Bookkeeping helps businesses track their profits and growth. It helps them assess their income and expenses, recognize patterns, and make informed decisions about how to allocate resources and where to focus their efforts. For example, if you see that your expenses are higher than your income, you may need to take steps to reduce costs or increase sales to improve your financial position.

Better Cash Flow Management

Accurate Bookkeeping also helps improve your business’s cash flow. With a complete understanding of your cash inflows and outflows, you can make the right decisions regarding where to invest, when to invest and how to manage bills, etc.

Bookkeeping gives you a clear picture of how cash is moving in and out of your business, enabling you to increase cash flow, forecast your finances, find ways to slash business costs and identify growth opportunities.

Financial Tracking

Effective Bookkeeping enables businesses to track their finances in real-time, providing visibility into cash flow, income, and expenses. By staying informed about their financial position, business owners can make timely and informed decisions to optimize their financial resources and reduce risks.

Financial tracking, also known as expense tracking, is the process of keeping tabs on your income and spending, ideally on a daily basis. It’s achieved by recording receipts, invoices and business expenses on an accounting ledger as well as tracking your finances goes hand in hand with creating a business budget.

Make Informed-business decisions

A well-maintained bookkeeping system provides businesses with the data necessary for doing business analysis and generating insightful reports that drive strategic decision-making. With the help of financial information recorded in the general ledger accounts, businesses can produce a variety of reports tailored to their specific business needs. These reports may include profit and loss statements, balance sheets, cash flow, forecasts & budgeting, etc.

Reporting & Analysis

With effective Bookkeeping, you can get accurate financial reports for your business and check the current status of your accounts. Financial reporting and analysis is the process of collecting and tracking data on a company’s finances on a monthly, quarterly, or yearly basis. Businesses use them to inform their strategic decisions, gain new investors, and comply with tax regulations.

Manual Bookkeeping vs Accounting Software

Manual Bookkeeping involves recording business transactions and figures to hand, typically in ledgers or journals. While this traditional method may seem labor-intensive, it offers a hands-on approach that allows business owners to have a deep understanding of their financial data. Manual Bookkeeping can be cost-effective for small businesses with straightforward financial needs, requiring minimal investment in software or training.

Using Accounting software, your data can be encrypted and protected by firewalls. It streamlines the bookkeeping process, automating many tasks and providing real-time insights into a business’s financial health. With features such as automatic transaction categorization, bank reconciliation, and customizable reporting, accounting software saves time and reduces the risk of errors associated with manual data entry. These cloud-based accounting solutions offer accessibility and collaboration capabilities, allowing business owners to manage their finances anytime, anywhere.

In-house vs Outsourced Bookkeeping

In-house Bookkeeping offers more personalized service since they are familiar with your company’s financial operations. Managing bookkeeping tasks in-house gives business owners direct control and oversight over their financial records. With the help of an internal bookkeeping system, businesses can ensure that financial information is readily accessible and aligned with their operational needs.

In-house Bookkeeping allows seamless integration with other business processes as well as provides immediate access to your financial information which can be crucial for day-to-day financial management and reporting.

On the other hand, Outsourced bookkeeping services refer to hiring an external service provider, typically for small businesses with limited resources. Outsourced bookkeeping firms bring specialized knowledge and experience to the table, ensuring proper bookkeeping practices and compliance with accounting standards.

Outsourced Bookkeeping is more cost-effective than hiring full-time personnel and more flexible to scale your operations up or down as needed. Outsourced bookkeeping firms may be a good choice for businesses that need more flexibility in terms of their services and rates.

Bookkeeping Services for Small Businesses

Bookkeeping is the process of categorizing all your income and expenses into a clear reporting structure. It can help you to stay organized and on top of your finances. Professional bookkeepers prepare and track financial documents, including invoices and bills, and create financial statements to ensure the business is ready for tax season and other financial reporting requirements. Maintaining bookkeeping tasks is essential for the stability and success of all small-sized businesses. Below are the services you can avail:

- Recording Transactions: Experienced Bookkeepers help you to record all financial transactions in a journal and then posted or transferred to the ledger, including sales, purchases, expenses, and payments, ensuring that every transaction is accurately documented.

- Bank Reconciliation: Bookkeepers reconcile bank statements with accounting records to ensure that all transactions are accounted for and identify any discrepancies in your company’s records, preventing fraud and theft from your bank account.

- General Ledger Maintenance: This is the process in which bookkeepers record, classify, and summarize financial transactions in a structured manner for easy access and analysis. It involves maintaining accurate and up-to-date records of economic activities, including accounts payable and receivable, assets, liabilities, and equity.

- Financial Reporting: Bookkeepers generate comprehensive financial reports, including profit and loss statements, balance sheets, and cash flow statements, providing valuable insights into the business’s financial performance and health.

- Tax Preparation and Compliance: Bookkeeping services often include assistance with tax preparation and compliance, ensuring that businesses meet their tax obligations with laws and regulations. The process includes timely filing of tax returns, accurate tax calculations, and applying the appropriate accounting methods.

- Financial Analysis: Bookkeepers help small business owners evaluate businesses, projects, budgets, and other finance-related transactions to determine their performance and suitability. A financial analyst will thoroughly examine a company’s financial statements—the income statement, balance sheet, and cash flow statement.

- Business Advisory: Bookkeeping services focus on your day-to-day operations, analyzing historical data and trends, and providing guidance, expert recommendations, and strategies to help business owners achieve their financial and operational goals.

Conclusion

Bookkeeping is an essential aspect of running a successful business. It not only helps in maintaining organized and accurate financial records but also plays a vital role in financial planning, compliance with tax laws, and informed decision-making.

Bookkeeping is the backbone of your accounting and financial systems, and it can impact the growth and success of your small business. It lets you know how you’re doing with cash flow and how your business is doing overall. Small business bookkeeping encompasses a variety of day-to-day tasks, including basic data entry, categorizing transactions, managing accounts receivable, and running payroll.