Service revenue is not an asset. It is classified as operating revenue and appears in the company’s income statement.

What’s covered in the article

A company’s total revenue comprises operating revenue and non-operating revenue.

Operating revenue means income generated from core business activities. Non-operating revenue means income generated from activities that are not a business’s basic objectives or non-core activities.

Some examples of operating revenue accounts are:

- Revenue earned from rendering services:

Example: revenue generated by tax accountants by providing tax advice; professional services rendered by advertisers, doctors, mechanics, etc.

- Revenue generated from product sales:

Example: sale of goods by manufacturing companies like sale of cars by car manufacturers.

Some examples of non-operating revenue accounts are:

- Revenue generated from the sale of assets, the difference in foreign exchange.

- Interest income, dividend income, etc. Gain on investments by a company not related to the investment business.

A business’s service revenue refers to the “top line” and is also called sales revenue contributing to the company’s net income.

After establishing the answer to the question, “is service revenue an asset” let us move forward and learn more about service revenue in detail.

What is Service Revenue?

Service revenue is generated as a part of sales revenue by rendering services for which the business is incorporated. Service can be rendered to anyone, but it should form one core business activity for generating economic value for the company.

If a business has more than one service, all the services performed will contribute to a single service revenue account. For example, a management consultancy firm can provide various services like:

- Industry analysis

- Tax advisory

- Mergers and acquisitions advice

- Valuation, etc

All the above services form the company’s primary source of income and will appear in the service revenue account.

Revenue recognition for service revenue is based on the accrual accounting method. The accountant records service revenue based on when the transaction occurs, irrespective of whether the cash is received.

In accrual accounting, the double entry system will create a debtor or accounts receivable from whom the payment is pending for which the service is already rendered.

Service revenue appears on the top of the business’s income statement because it is a part of operating revenue. The cash, credit, and deferred payment settlements will reflect in the company’s balance sheet. But the obligation to perform service or receive a payment within an accounting period will be reflected in the income statement.

Due to the double entry system, the counter portion of the operating income will be shown either as cash, accounts receivable or deferred revenue.

What are the Types of Service Revenue?

Operating revenue is a major portion of a company’s net income. Service revenue is recognized when the activity that generates the revenue must be either the core business operation or a part of the core business operation.

Example: If a manufacturing company invests in the money market and earns interest income, then this income will be shown in the income statement as non-operating income. In comparison, an investment firm’s interest in money market instruments will be treated as its operating income.

In a service-oriented revenue model, there are the following common ways of generating service revenue:

- Customer support service revenue: Services include troubleshooting, installing, assembling, delivering, annual maintenance contracts, upgrading, etc.

- Customization/ processing: Service revenue is generated from providing customization services like car modifications, custom-fit clothes, etc., and processing services like dry cleaning, paint job, etc.

- Recurring payment: Service revenue is generated periodically, like subscription fees for gyms, OTT platforms, magazines, etc.

- Licensing and franchisee revenue: License and franchisee fee earned by the franchisor from franchisees.

- Consulting fees: Service revenue earned from providing consultations like legal, management, medical, etc.

- Outsourcing support: Service revenue generated by providing outsourcing services like KPO services.

- Digital services revenue: Service revenue generated from digital services performed like IaaS (Infrastructure as service), PaaS (Platform as a service), FaaS (Function as a service), SaaS (Software as a service), etc.

How is Service Revenue Recorded on a Balance Sheet?

Service Revenue Recognition

Revenue recognition in accrual accounting is based on the principle of obligation. When a service is rendered, there is an obligation on the part of the consumer to pay.

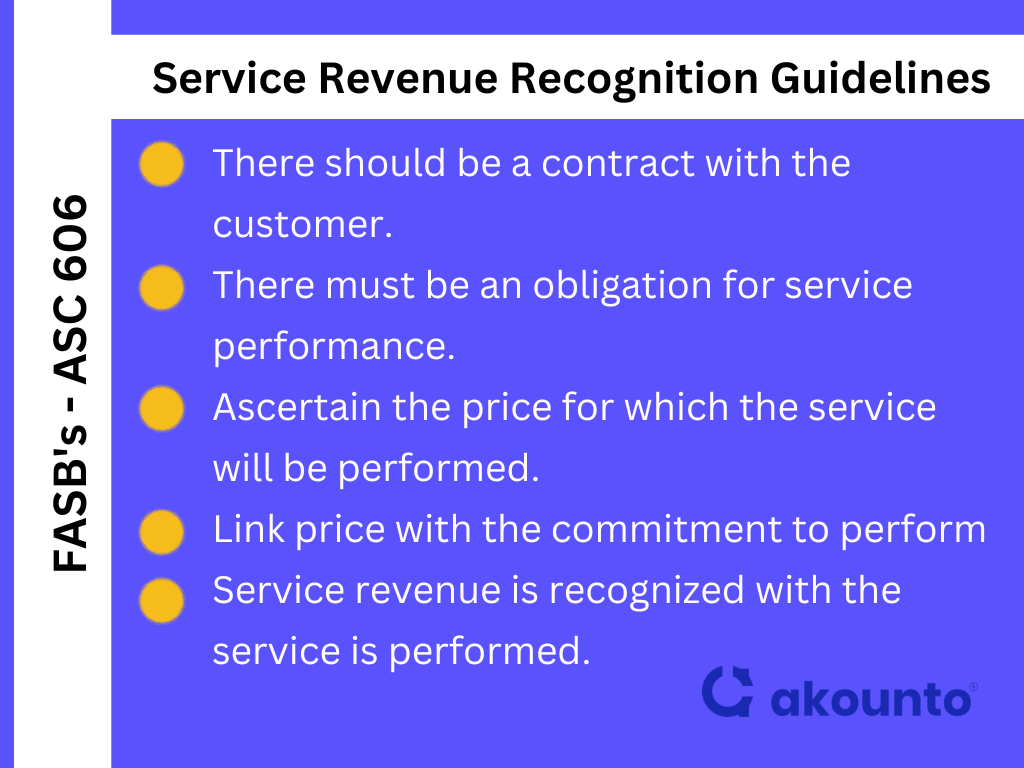

FASB (Financial Accounting Standards Board) has released revenue recognition standard ASC 606 (Accounting Standard Codification), which lays down the following framework to recognize revenue from contracts with customers:

- There should be a contract with the customer.

- There must be an obligation for service performance.

- Ascertain the price for which the service will be performed.

- Link price with the commitment to perform

- Service revenue is recognized with the service is performed

Service Revenue Bookkeeping Entries and Balance Sheet Reporting

The balance sheet comprises assets and liabilities along with shareholders’ equity. Service revenue appears indirectly on a business’s balance sheet, either as accounts receivable or as an unearned income to whom the company owes service performance. Accrual accounting records the obligations irrespective of cash settlement.

Sample balance sheet:

Akounto Help Center Inc.Balance Sheet as of Month xx xxxx

| Assets | Amount ($) | Liabilities | Amount ($) |

| Current assets | Current liabilities | ||

| Cash | 5021 | Accounts payable | 6472 |

| Marketable securities | 2564 | Unearned revenues | 2786 |

| Inventory | 8940 | Warranty liability | 1200 |

| Accounts receivable | 2345 | ||

| Total current assets($) | 18,870 | Total current liabilities ($) | 10,458 |

| Fixed assets | Long term liabilities | ||

| Land | 7,800 | Bank loan | 75,000 |

| Buildings | 1,50,000 | Stockholders’ equity | |

| Equipments | 7,000 | Common stock | 100,000 |

| Goodwill | 3250 | Reserves and surplus | 1462 |

| Total assets | 186,920 | Total liabilities and stockholders’ equity | 186,920 |

Accounts receivable will be a current asset account with a debit balance, while unearned income will be a current liability account with a credit balance. In both cases, the income statement will also reflect the obligation to receive or already receive the payment.

The general format for service revenue journal entry is:

Basic Journal Entry Format

| Date | Cash (Debit) | xxx |

| To Service Revenue (Credit) | xxx |

Case 1: The case of a normal cash-settled service revenue transaction:

The above format is applied when the business renders service to the customer and receives payment. Then the service revenue is an operating revenue that will appear on the top of the income statement.

Example: John went to a men’s salon and got a haircut for $ 100 on May 21. He paid after getting the service. The salon will pass the following journal entry to record service revenue:

Cash Payment in Return for Service – Journal Entry

| May 21 | Cash (Debit) | 100 |

| To Service Revenue (Credit) | 100 |

Case 2: The case of credit sales where accounts receivable is created

When a customer avails of the actual service, the payment is due. The customer is obliged to pay, while the company has the right to receive the payment. Thus, under the rules of accrual accounting, service revenue will be recorded by creating accounts receivable in the customer’s name.

The customer as accounts receivable will have a debit balance while the company will record service revenue, and there will be no additional cash flow.

Example: John gets the hair job done for $ 100 on May 21 but promises to pay later. The journal entry will be:

Credit Sales Resulting in Creating Accounts Receivable – Journal Entry

| Date | Particulars | Debit ($) | Credit ($) |

| May 21 | Accounts Receivable (John’s A/C) (Debit) | 100 | |

| To Service Revenue (Credit) | 100 |

Case 3: The case when the customer pays in advance and unearned revenue is created:

When a consumer pays in advance, it becomes deferred revenue for the company, also known as unearned revenue. The customer becomes a creditor to whom the company has the debt due to the payment being received in advance. The company has an obligation to render services.

In the case of unearned revenue, the cash flow statement helps gauge revenue collection efficiency.

Example: John calls the salon on May 21 and pays $ 100 as a booking amount for a service he wishes to avail next month. The journal entry will be:

Advance Payment Creating Unearned Revenue – Journal Entry

| Date | Particulars | Debit ($) | Credit ($) |

| May 21 | Cash (Debit) | 100 | |

| To Unearned Revenue Account (John’s A/C) (Credit) | 100 |

Final Words

When the question is asked, “is service revenue an asset” then it must be noted that asset helps generate revenue, while asset themselves are not revenue. Service revenue is operating revenue and a part of the company’s total revenue and net income.

Revenue recognition is important for small business accounting because it impacts profit computation, taxation, and the accuracy of financial statements. Wrong or mistaken revenue recognition can result in untrue and misleading financial statements.