What is an Operating Lease?

An operating lease is a contract where the right to use an asset for a particular period is given, but not its ownership rights. The main advantage of operating lease is to use an asset without purchasing it.

The asset is returned to the lessor/ owner/ finance at the end of the lease term.

What’s covered in the article

Buying an asset involves paying a very high upfront cost, which may not leave funds available for other purposes like business expansion, purchasing other assets, etc. With an operating lease, a business can get costly assets at a low monthly lease payment.

Typically, businesses rent vehicles, machinery, real estate, aircraft, etc.

Before moving further, let us define a few jargons for ease of understanding:

- Lessee: The lessee can be a “business” or an “individual” who is basically a “tenant” who has taken the asset on rent.

- Lessor: The party, i.e., “person” or “business,” that owns the asset or has the “ownership rights.” The lessor rents the property or asset to the lessee (tenant),

- Leased Asset: Leased asset refers to the asset that has been given to the tenant for use for a specific period against monthly payments. A leased asset is also known as the underlying asset for which the lease contract is made. In lease accounting, the leased asset is also called an ROU asset (Right of use asset).

- Lease Term: The lease term is the period for which the underlying asset is given on rent (leased) to the tenant (lessee) by the owner (lessor) for monthly payments (lease payments).

- Lease Payments: It is a fixed monthly payment for the asset taken on rent. The asset belongs to the “lessor”; the person who has taken on rent is called the “lessee.”

- Lease Contract: A lease contract is a legally enforceable lease agreement that defines terms and conditions regarding the use of the underlying asset, clearly mentions the lease term, and gives the monthly rental payments and obligations of the lessor and lessee.

- Residual Value: It is the market value or the estimated value of the underlying asset when the lease expires or at the end of the lease term.

Merits of Operating Lease for Small Businesses

- Small business owners can get expensive assets for lower monthly operating lease payments. Operating leases help businesses to save money and get the much-needed asset when they are already tight on cash.

- Operating leases are especially effective where the useful life or the economic life of the expensive assets is short, as owning the asset is commercially not feasible in that case.

- Operating leases are beneficial where the lease contracts are for less than a year, as then the lease liability can be shown as an operating expense in the financial statements.

- In the growth and expansion phase of the business, operating leases get more for every dollar spent. As the businesses have to pay a lower monthly sum for the leased assets and can get the work done otherwise, the upfront payment to buy the asset could have diverted the funds from other critical business activities.

- Operating leases are beneficial since the ownership is not transferred, and the legal representation of other formalities related to the asset rests with the lessor. This makes the ROU hassle-free.

- There are tax benefits from operating leases where the monthly payments are shown as operating expenses, thereby reducing the taxable income.

How Does Operating Lease Work?

Operating leases are usually for a shorter term and subsume the renting process. It gives the right of use without ownership transfer. The lease contract between the lessor and the lessee defines the terms and conditions for the lease, including the lease payments, lease terms, conditions of use, and sometimes even maintenance and repairs.

Previously, the operating lease used to be an off-balance sheet item, thereby keeping the debt-to-equity ratio low. However, after the transition from ASC 840 to ASC 842, there are specific conditions where the operating lease becomes part of the company’s balance sheet.

Example of Operating Lease

Example:1

In post-covid times, the most common example of an operating lease can be a “co-working space.

A small business owner employs 10-15 employees, but buying a floor in a commercial office building can be very expensive and even unaffordable. Taking the floor or some rooms in the building can be affordable, and the business owner has to make monthly payments.

Example:2

A builder is developing real estate, and for construction, a high-powered generator is needed. It is much more feasible to take the generator for rent for his projects than to pay a very high upfront cost. The lease expense can reduce the taxable income while the asset will be returned to the owner in the same condition as it was received at the end of the lease period.

Operating Lease Accounting

For accounting purposes, the lease agreement is shown in the balance sheets of both the lessor and the lessee.

In 2016, the FASB (Federal Accounting Standards Board) issued Accounting Standard Update (ASU) 2016 concerning ASC Topic 842, Leases, which significantly impacted operating lease accounting.

According to ASC 842, the lessee must classify the lease either as a finance lease or an operating lease.

In the case of finance leases, the interest and amortization expenses are recognized, while they are not recognized in the case of a short-term single lease on a straight-line basis.

As per ASU 2016, if the lease term is for less than 12 months, then the lessee can show it as an expense using the straight-line basis method. If the lease term is for more than 12 months, then the lessee must recognize it as a lease liability and an ROU asset on the balance sheet.

Further, FASB issued ASU 2021-05 in July 2021, where the lessors of the leases have to classify a lease with variable payments (not following any index rate) as an operating lease when the lease can be recognized as a direct financing lease or sales-type lease according to the criteria laid down by ASC 25-3, ASC 842-10-25-2.

The lessor recognizes the variable payments in the income statement of the company as when they are incurred, while periodic lease payments are recognized on a straight-line basis. The initial cost of purchasing the asset is accounted for the life of the lease.

In ASU 2021-09 (issued in 2021, November), permitted non-PBEs (Public Benefit Entities) lessees to use a risk-free discount rate to measure and classify leases. They can also select the accounting policy on the basis of the class of the assets leased and not on the basis of the type of company.

(Note: ASU 2016 and ASC 842 are not applicable to the following arrangements: Intangible asset leasing; Exploration for or use of nonregenerative resources; Biological assets leases; Inventory leases; Assets under construction)

Demerits of Operating Lease

- No ownership leads to no buildup of equity in the case of operating leases. The business does not own the asset at the end of the lease period, which could have been an asset on the company’s balance sheet. However, after paying for the full term, the lessee does not get the asset (as happens in a finance lease).

- There is no benefit of off-balance sheet financing, as the changes in the accounting guidelines have mandated the recognition of the lease arrangement on the company’s financial statements.

- Operating leases can be costly in the long run, where the monthly payments are made, and still, the asset is not acquired. Also, the total lease payments could be more than the present value of the underlying asset since they also include finance charges.

- The finance can opt not to renew the lease at the end of the term, so there can be a risk if the firm uses a heavily leased model of financing.

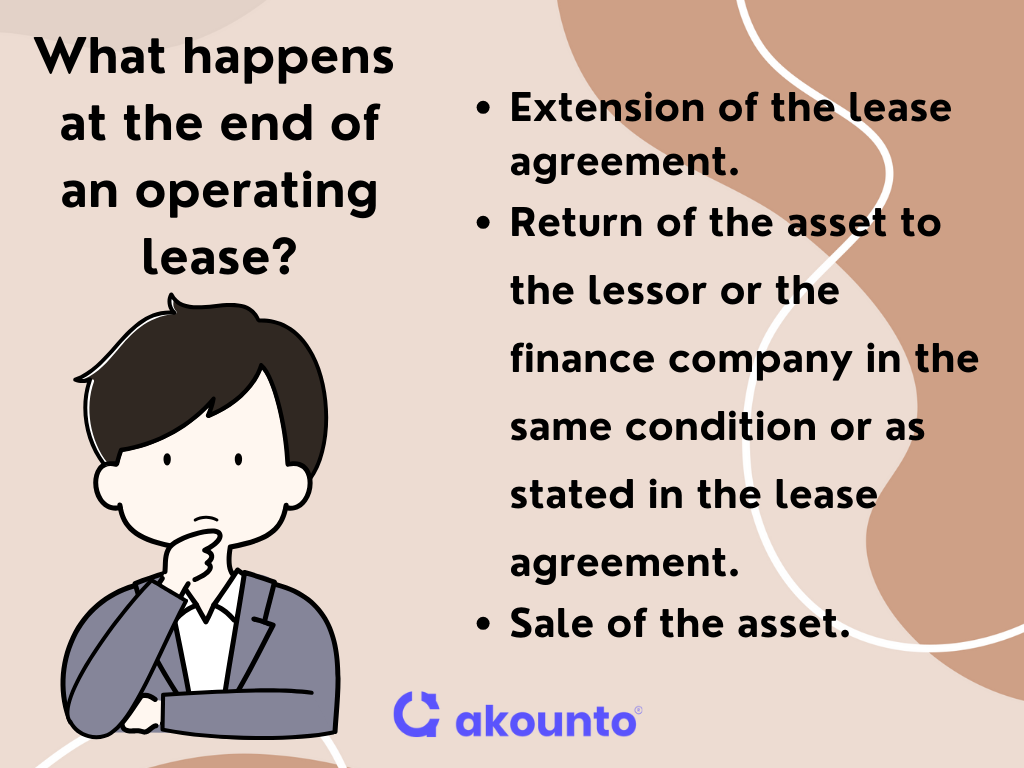

What happens at the end of an operating lease?

At the end of the lease term, as stated in the lease agreement, any one of the following things can happen:

- Extension of the lease agreement.

- Return of the asset to the lessor or the finance company in the same condition or as stated in the lease agreement.

- Sale of the asset.

When the lease term ends, then the ROU asset is assessed for its residual value. The underlying asset is sold to the third party. If the selling price is more than the residual value, then the lessee will get the surplus amount. If the selling price is lower than the residual value, then the lessee will have to pay the difference to the lessor or the finance company.

Other Types of Leases

Finance Lease:

A finance lease is also known as a capital lease, where the ownership of the underlying asset is transferred to the lessee at the end of the finance lease term. A small business owner must know the difference between a capital lease and an operating lease to take better advantage of the financing options.

Sales and Lease Back

The sale and leaseback arrangement is where the seller (lessee) sells the asset to the buyer (lessor) and then leases it back with the right of use for a certain lease term.

Single Net Lease

A single net lease refers to an agreement (usually in real estate lease agreements) where the lessee pays taxes along with the rent.

Double Net Lease

Double Net Leases are also called Net-Net leases, where the tenant or the lessee pays insurance premiums and property taxes in addition to the monthly rent.

Tripple Net Lease

Tripple Net Lease, also known as NNN Lease, where the lessee or the tenant pays taxes, insurance, and maintenance in addition to the monthly payments.

Ground Lease

Ground lease, also known as land lease, is usually for 50 to 99 years, where the lessee or tenant takes land on rent, develops and uses the structure he built, and then returns the same at the end of the lease term.

Gross Lease

In a Gross Lease, the tenant pays a flat fee, and the landlord takes care of other expenses. Basically, the rent includes other expenses.

Subleases

Sublease is an arrangement where the lessee leases the underlying asset to a third party and becomes an immediate lessor. But the original agreement between the lessee and the lessor stays in effect.

Conclusion

Operating leases can be a very smart financing option for an emerging small business where the cash is limited, and the asset in need is only for a short time and is very costly. In such cases, an outright purchase is not commercially feasible. An operating lease is more of a strategic decision than an operating decision that impacts both in the long run as well as in the short-run.

Get more knowledge and tips that are helpful for small business owners at Akounto’s blog.