What are Accounting Errors?

Accounting errors are mistakes or inaccuracies that occur while recording, classifying, summarizing, and interpreting financial transactions and information.

What’s covered in the article

These accounting mistakes can occur due to human error, faulty systems, incorrect reporting, unintentional mistakes, or deliberate employee fraud.

Accounting errors impact financial statements, affecting decision-making, financial analysis, and compliance with regulatory requirements.

Identifying and rectifying these errors is crucial for maintaining financial records’ integrity and ensuring the business’s books are accurate and according to accounting practices.

Detecting accounting errors requires scrutiny of financial records, including the bank statement, trial balance, and general ledger entries. Regular reconciliations, reviews, and audits can help find accounting errors, discrepancies, and inconsistencies.

Preventing accounting errors involves:

- Implementing robust internal controls, such as segregation of duties.

- Regular training and education for accounting staff.

- Implementing accounting software with built-in error-checking mechanisms.

- Adhering to generally accepted accounting principles (GAAP).

By understanding the types, causes, detection methods, and prevention strategies related to common accounting errors, small businesses, entrepreneurs, and freelancers can minimize the risks associated with inaccuracies in their financial records and ensure the reliability of their accounting information.

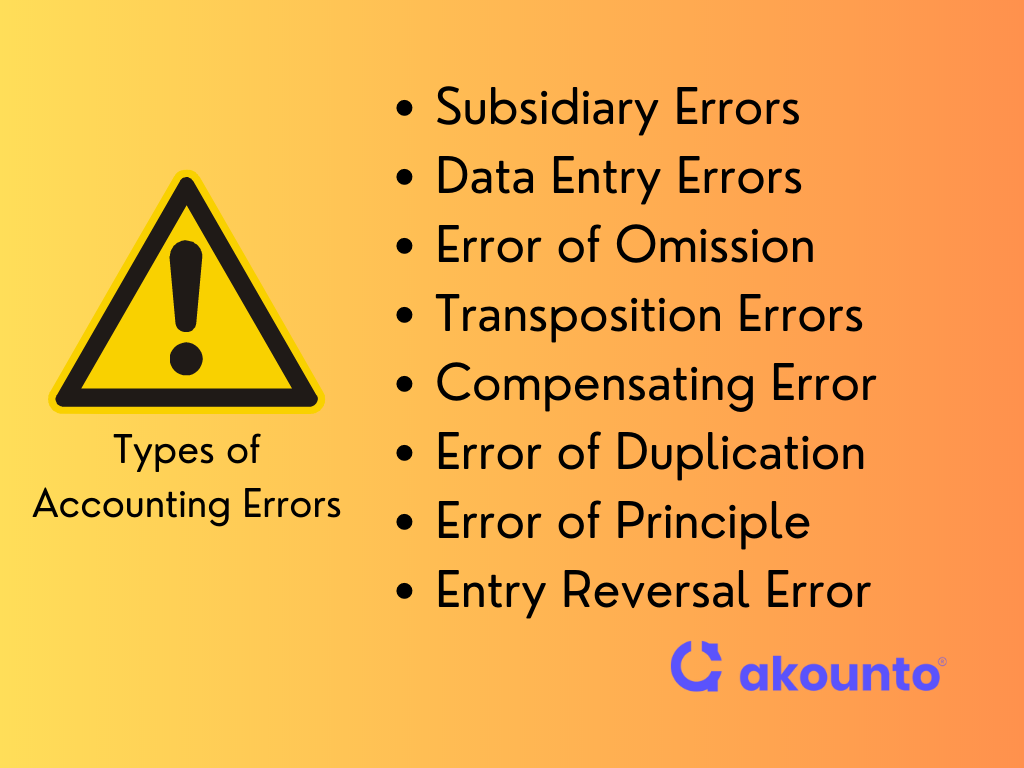

Types of Accounting Errors

Accounting errors affect the accuracy and reliability of financial reports and can lead to penalties in case of a tax audit. Let’s explore the most common accounting errors, along with examples:

Subsidiary Errors

Subsidiary errors are mistakes that arise due to errors in subsidiary books or subsidiary records. These errors can impact the accuracy of ledger accounts and financial books. For instance, recording a sale in the subsidiary sales book but failing to transfer it to the general ledger results in an omission error.

Example

Company XYZ recorded a credit sale of $1,000 in the subsidiary sales book but failed to update the accounts receivable account in the general ledger.

Data Entry Errors

Data entry errors occur when incorrect data is inputted into accounting systems or spreadsheets. These errors can arise from transposing numbers, omitting digits, or entering incorrect amounts. Data entry errors can lead to discrepancies in financial calculations and reports.

Example

While making an accounting entry, the accountant mistakenly enters a payment of $1,500 as $15,000, resulting in an overstatement of expenses and an understatement of cash on the balance sheet.

Error of Omission

The error of omission is an accounting error where the accountant fails to record a financial transaction or entry. This is the most common accounting error.

Omission errors occur when a transaction is completely left out or omitted from the accounting records, leading to an imbalance and inaccurate financial statements.

Example

Company ABC forgot to record a payment received from a customer for $2,000, resulting in an understatement of accounts receivable and an overstatement of income.

Error of Commission

The error of commission happens when incorrect accounting transactions are recorded due to human error or misinterpretation of information. This type of error involves recording a transaction but entering incorrect amounts, in a wrong account, or incorrect details.

Example

An accountant mistakenly records a payment to a supplier as an expense instead of accounts payable, resulting in an overstatement of expenses and an understatement of liabilities.

Transposition Errors

The transposition error occurs when digits or numbers are unintentionally reversed when recording financial data. This error often happens during manual data entry, leading to inaccurate calculations and financial records.

Example

A bookkeeper records a payment of $1,890 as $1,980 due to the accidental transposition of digits, resulting in an incorrect balance in the accounts receivable account.

Compensating Error

Compensating errors are two or more errors that offset each other, resulting in a net effect of zero on the financial books. This type of accounting error can go unnoticed if they cancel each other out, but they can still impact the accuracy of individual accounts and will not be detected by trial balance totaling.

Example

Company PQR overstates its accounts receivable balance by $1,000 but simultaneously overstates its sales revenue by the same amount, resulting in an offsetting effect on the financial books.

Error of Duplication

Duplication error occurs when a transaction or entry is recorded multiple times in the accounting records. It can lead to overstating or understating account balances and distorting financial reports.

Example

An accountant accidentally records a sales invoice twice, resulting in an overstatement of revenue and accounts receivable.

Error of Principle

The principle error refers to a violation of accounting principles or practices. It occurs when a transaction is recorded using an incorrect accounting method, resulting in an inaccurate representation of the financial position and performance of the business.

Example

A business capitalizes an expense that should have been treated as a revenue expenditure, leading to an incorrect allocation of costs and an overstatement of assets.

An Entry Reversal Error

The error of entry reversal happens when a transaction is recorded with the opposite direction or sign than intended. It occurs when debits are mistakenly recorded as credits and vice versa. This error can impact the accuracy of account balances and financial books.

Example

Company LMN records a payment received from a customer as a credit instead of a debit in the accounts receivable account, resulting in an understatement of receivables and an incorrect representation of the customer’s outstanding balance.

Causes and Detection

Accounting errors can arise from various factors, including human error, system glitches, misinterpretation of information, and inadequate internal controls.

Understanding the causes of accounting mistakes is crucial for implementing effective detection and prevention measures.

Causes of Accounting Errors

- Human Error: Mistakes made by individuals during data entry, calculations, or interpretation of financial information can lead to accounting errors. Fatigue, lack of training, distractions, or simple oversight can contribute to human errors.

- Inadequate Internal Controls: Weak internal controls increase the risk of accounting errors. Lack of segregation of duties, insufficient oversight, and inadequate review processes can create opportunities for errors to go undetected.

- System Malfunctions: Accounting software or systems can experience glitches, bugs, or technical issues, resulting in incorrect calculations, data corruption, or faulty entries.

- Misinterpretation of Information: Misunderstanding or misinterpreting accounting principles, guidelines, or transaction details can lead to errors in recording or classifying financial transactions.

- Time Pressure: Working under tight deadlines or rushing through tasks can increase the likelihood of errors. Insufficient time for proper review and verification can result in overlooked mistakes.

Detection of Accounting Errors

- Regular Reconciliations: Conducting regular reconciliations, such as bank reconciliations, ensures that recorded transactions match external sources, such as bank statements. Discrepancies can indicate errors that need to be addressed.

- Trial Balance Review: Regularly reviewing the trial balance helps identify imbalances between debit and credit totals, highlighting potential errors in the general ledger.

- Analyzing Financial Statements: Careful analysis of financial books, including statements of profit and loss, balance sheets, and cash flow statements, can reveal inconsistencies or unexpected fluctuations that may indicate errors.

- Independent Reviews and Audits: Periodic independent reviews and audits by external professionals provide an unbiased assessment of financial records, helping to identify errors or irregularities.

- Error-Checking Mechanisms: Utilizing accounting software with built-in error-checking mechanisms can automatically flag potential errors, such as unbalanced journal entries or incorrect account coding.

- Segregation of Duties: Implementing a system of checks and balances by separating individual responsibilities helps detect errors and prevent fraudulent activities.

- Thorough Documentation and Documentation Review: Maintaining comprehensive documentation of financial transactions and conducting regular reviews of supporting documents can help identify discrepancies and errors.

Impact on Financial Statements

Accounting errors can have significant implications for the accuracy and reliability of financial statements. These errors can distort business finances, leading to under or over-reporting.

Understanding the impact of accounting errors on the statements is crucial for assessing the true financial position of a company.

- Income Statement: Accounting errors can affect the income statement by misrepresenting revenue, expenses, and, ultimately, the net income of a business. Errors in revenue recognition can lead to overstated or understated revenue figures, thus distorting the company’s profitability. Similarly, misclassification or omission of expenses can result in inaccurate expense reporting, affecting the calculation of net income.

- Balance Sheet: Errors in the balance sheet can impact the reporting of a company’s assets, liabilities, and equity. For example, misstating the value of an asset or liability can affect the accuracy of the balance sheet and mislead stakeholders about the company’s financial position. Inaccurate reporting of accounts receivable or accounts payable can distort the liquidity and solvency analysis of the business.

- Cash Flow Statement: Accounting errors can also affect the cash flow statement, which provides insights into a company’s cash inflows and outflows. Cash flow categorization errors or misrepresenting cash transactions can lead to misleading information about a company’s operating, investing, and financing activities, impacting cash flow analysis and financial decision-making.

- Financial Ratios and Analysis: A single accounting error can distort key financial ratios used for performance evaluation, such as profitability ratios, liquidity ratios, and debt ratios. Inaccurate financial ratios can misguide investors, lenders, and other stakeholders in assessing the company’s financial health and making informed decisions.

A business owner must lay down an accounting system to identify common errors to ensure the accuracy and reliability of financial books. It could be the utilization of trial balance, matching business receipts with accounting transactions, etc.

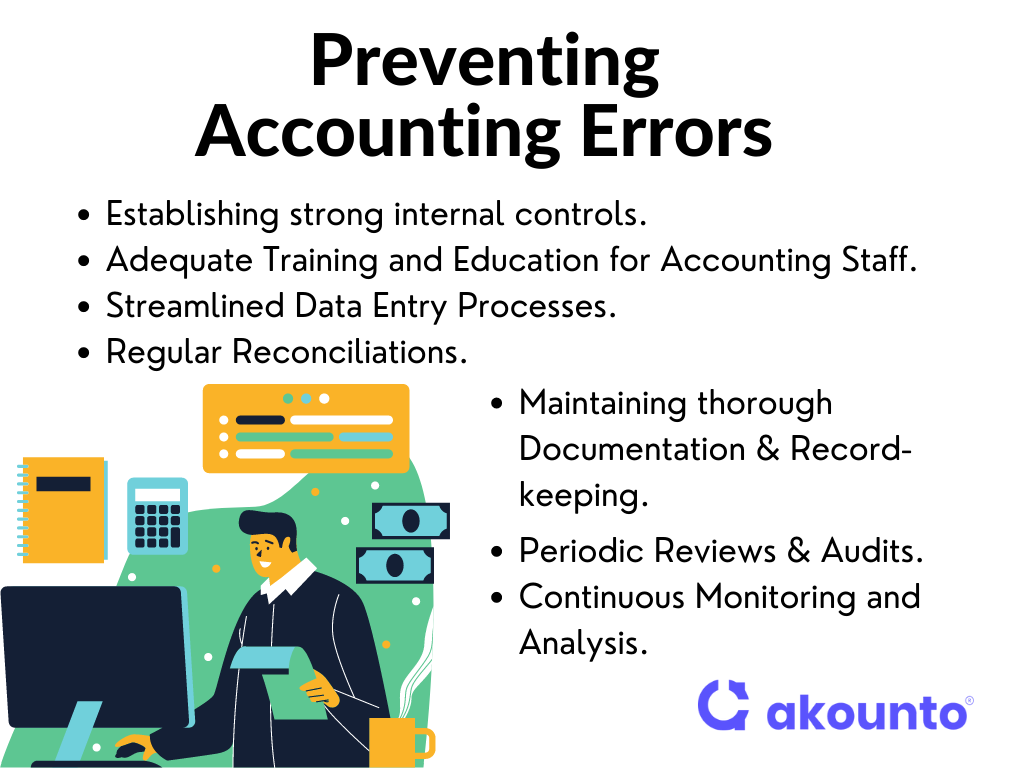

How to Prevent Accounting Errors?

Implementing effective strategies and controls can significantly reduce the occurrence of errors.

- Robust Internal Controls: Establishing strong internal controls is crucial in preventing accounting errors. This includes implementing segregation of duties, defining accounting rules and policies, authorization for certain business expenses, and an accounting process that maps all accounting entries.

- Adequate Training and Education: Investing in comprehensive training programs for accounting staff is essential. Ensuring employees understand accounting principles, procedures, and software systems can minimize errors caused by a lack of knowledge or skills. Ongoing training programs can keep accounting professionals updated with the latest regulations and best practices.

- Streamlined Data Entry Processes: Implementing streamlined data entry processes, such as using accounting software with built-in error-checking features, can minimize errors caused by manual data entry. Most accounting software can automatically flag potential errors, such as unbalanced journal entries or incorrect account coding, reducing the risk of transcription mistakes.

- Regular Reconciliations: Regular reconciliations, such as bank reconciliations, helps identify discrepancies between recorded transactions and external sources. This ensures that errors are identified and resolved promptly, maintaining the accuracy of financial records.

- Documentation and Record-Keeping: Maintaining thorough documentation and record-keeping is crucial for accurate accounting. Properly documenting financial transactions and maintaining supporting documents can help trace and rectify errors. It also provides a reliable audit trail for future reference.

- Periodic Reviews and Audits: Conducting periodic reviews and audits of financial records by internal or external professionals can help identify errors and ensure compliance with accounting standards. Independent assessments provide an unbiased perspective on the accuracy and integrity of financial records.

- Continuous Monitoring and Analysis: Regularly monitoring and analyzing financial data can help identify patterns, trends, and anomalies that may indicate errors. Financial analysis tools and software can streamline this process and enhance error detection.

Conclusion

Accounting errors can have significant consequences for businesses, ranging from financial misstatements to inaccurate decision-making. It is essential for small business owners, entrepreneurs, and freelancers to understand the types of accounting errors, their impact the financial statement, and how to prevent them.

Implementing preventive measures, such as robust internal controls, comprehensive training programs, streamlined data entry processes, regular reconciliations, thorough documentation, periodic reviews and audits, and continuous monitoring, can significantly reduce the occurrence of accounting errors.

Use Akounto accounting software to effortlessly record your transactions and keep track of your accounts.