What are Liquidity Ratios?

Liquidity ratios are accounting ratios used to measure a company’s ability to pay its short-term financial obligations.

What’s covered in the article

Short-term creditors, lenders, and investors are keen to measure a company’s ability to pay its short-term debt obligations and to pay vendors. A healthy liquidity ratio signals the business’s ability to cover its short-term obligations without raising cash from external sources.

Liquidity ratio analysis assesses whether the company’s liquid assets can pay for its current liabilities. As the liquidity ratio measures a company’s ability to meet short-term obligations, the solvency ratio measures the company’s ability to meet long-term debt obligations.

Often liquidity ratios and solvency ratios are taken together to ensure the debt-servicing capacity of the company. Short-term and long-term debt obligations constitute the total financial obligations of a business.

This article will focus on understanding liquidity ratios in depth to measure and interpret a company’s liquidity.

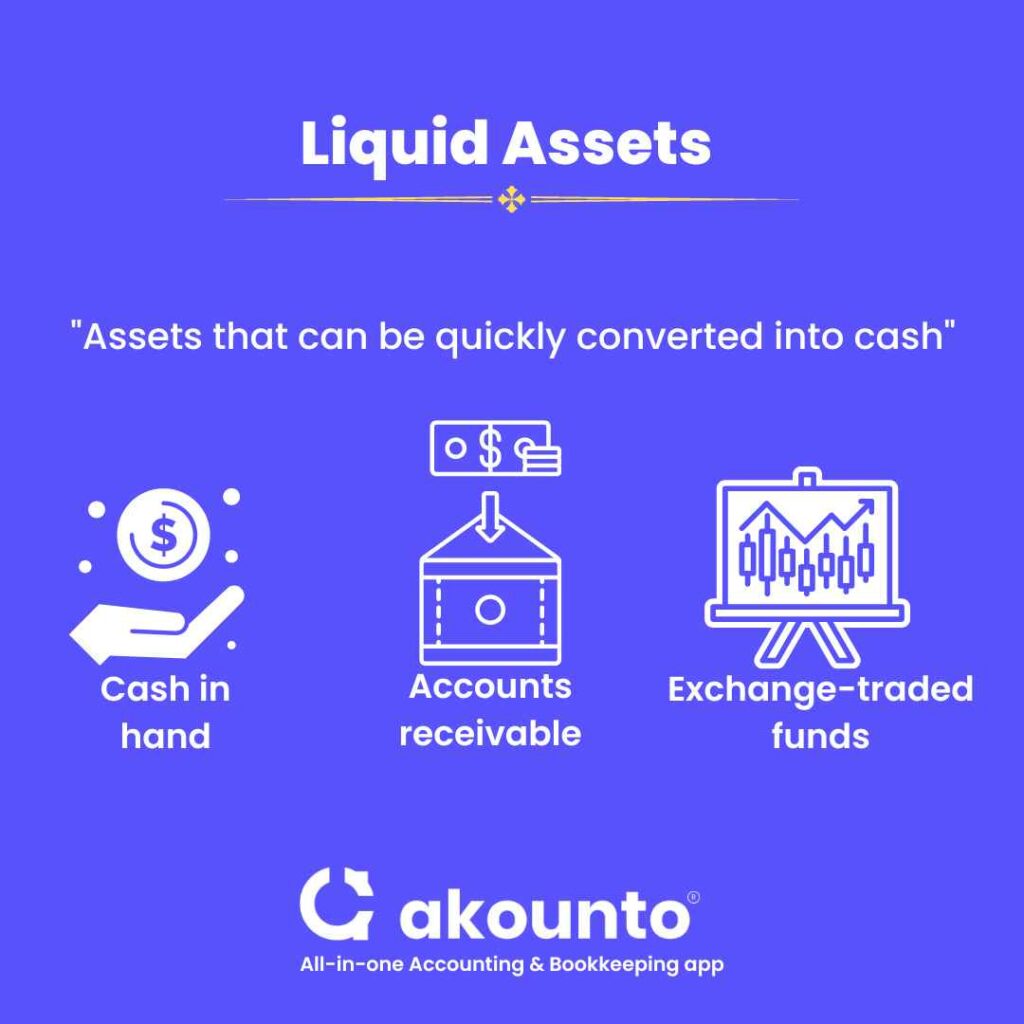

What are Liquid Assets?

Liquidity in accounting refers to the asset’s ability to be converted to cash quickly within a given time frame. Easier to convert an asset into cash, the more liquid it is.

In the balance sheets, liquid assets are recorded as part of current assets.

Liquid assets are normally cash equivalents or easily cash convertible at very short notice. Some examples of liquid assets are:

- Cash in hand

- Cash at bank

- Marketable securities

- Treasury bills

- Accounts receivable

- Fixed deposits

- Commercial papers like bills of exchange

- Certificate of deposits (CDs)

- Short term investments

- Bonds

- Exchange-traded funds

- Inventory

A company’s financial health in the short term is measured by the number of liquid assets on its balance sheet, ensuring a margin of safety to pay for short-term obligations and meet emergencies and distress in the short term.

Types of Liquidity Ratios

The following are the most common types of liquidity ratios generally used to measure a company’s financial health:

Current Ratio

Of all the common liquidity ratios, the current ratio (working capital ratio) is the broadest measure of a company’s liquidity, as it measures all the current liabilities against all the current assets on the balance sheet. Though the degree of liquidity differs amongst current assets, this overgeneralization helps in a broad inter-industry comparison but could be more helpful in intra-industry comparisons.

Cash Ratio

Cash ratio measures a company’s ability to pay for its current liabilities using only cash and cash equivalents. In comparison to the current ratio, the cash ratio takes into account only cash and cash equivalents and not all current assets. The cash ratio is considered the most conservative of all the liquidity ratios.

Acid Test Ratio (Quick Ratio)

The quick ratio is between the current ratio and the cash ratio. It includes cash and cash equivalents (like in the cash ratio formula) and other ‘quick assets’ like marketable securities and net accounts receivable. Quick assets do not include inventory and prepaid expenses.

Operating Cash Flow Ratio

This liquidity ratio measures the capability of the company’s regular cash-generating activities to meet its short-term debt obligations. Cash from operations is preferred in this ratio compared to the company’s net income.

How to Calculate Liquidity Ratios?

Current Ratio Formula

Current Ratio = Current Assets/ Current Liabilities

Current assets include all current assets, including inventories, accounts receivable, cash and cash equivalents, and other current assets.

Current liabilities are all the liabilities (debts, wages, interest payments, etc.) payable within an accounting period. This also includes the part of long-term liabilities that are meant to be paid in the current accounting year.

Cash Ratio Formula

Cash Ratio = Cash and Cash Equivalents/ Current Liabilities.

Holding cash is important to meet financial emergencies during a recession or other economic distress. In its numerator, the cash ratio only considers cash (in-hand and at the bank) and cash equivalents (near cash securities like bills of exchange). It excludes all other liquid assets like inventories, accounts receivables, etc. Less than one in a cash ratio signals insufficient cash in the company.

Quick Ratio Formula

Quick Ratio = Quick Assets/ Current Liabilities

Quick Assets = Total Current Assets – Inventory – Prepaid Expenses

In the numerator, there are ‘Quick assets” that are derived by excluding inventories and prepaid expenses from all the current assets. While for the denominator part, all the current liabilities are considered.

Operating Cash Flow Ratio Formula

Operating Cash Flow Ratio = Cash from Operating Activities/ Current Liabilities.

Cash from operations is highlighted in the cash flow statement of the company. Cash from operating activities represents the cash equivalent portion of net income.

Liquidity Ratios – Example

| ABC Inc. – Balance Sheet | |

| Assets | Millions |

| Cash | 170 |

| Marketable Securities | 50 |

| Inventory | 200 |

| Accounts Receivable | 160 |

| Prepaid Expenses | 120 |

| Total Current Assets | 700 |

| Land and Building | 330 |

| Total Assets | 1030 |

| Liabilities | |

| Current Liabilities | 200 |

| Long-term Debts | 260 |

| Shareholders’ Equity | 400 |

| Retained Earnings | 170 |

| Total Liabilities | 1030 |

Current Ratio = Current Assets/ Current Liabilities

Current Ratio = 700/ 200 = 3.5

The company has a very high degree of liquidity and could be saving surplus cash that could have been invested elsewhere.

Quick Ratio = Quick Assets/ Current Liabilities

Quick Assets = Total Current Assets – Inventory – Prepaid Expenses = 700 – 200 – 120 = 380

Quick Ratio = 380/ 200 = 1.9

Given the high current ratio, the quick ratio is also very high, almost double. The company can easily pay for all its current liabilities without selling any assets.

Cash Ratio = Cash and Cash Equivalents/ Current Liabilities.

Cash Ratio = (170 + 50)/ 200 = 220/ 200 = 1.1

The company holds enough cash to pay all its current liabilities in case it needs to pay immediately.

How to Interpret Liquidity Ratios?

- Current Ratio: Generally, a current ratio of 1 is considered a healthy liquidity ratio. It is interpreted as there is one current asset to cover one current liability. Though the current ratio also depends on the industry type. An FMCG (fast-moving consumer goods) is expected to have a higher current ratio than the heavy manufacturing industry.

- Cash Ratio: If a company has to pay all the existing debt obligations immediately with cash only, this ratio highlights the ability to pay without selling assets.

- Quick Ratio: The company’s ability to cover short-term obligations using cash and near-cash assets is highlighted in this liquidity ratio. Similar to the current ratio, the quick ratio of 1 is considered optimum. Less than one highlights insufficient cash, and the company can easily slide into distress if there are delays in the working capital cycle.

- Operating Cash Flow Ratio: A higher operating cash flow ratio means an adequate financial structure of the company. It also highlights that the company’s core business operations cannot meet its short-term liabilities.

What is Liquidity Crisis?

A company with a good liquidity ratio implies its creditworthiness in the short term. Investors, lenders, and creditors are interested in liquidity ratios to analyze money management in core terms.

Low liquidity ratios imply a shortage of funds, while a higher liquidity ratio signals a mismanagement of cash. Blindly following, the “higher the better” approach is also detrimental as there are opportunity costs for holding too much cash and risking inflation while foregoing opportunities for business growth.

Of all the financial ratios, liquidity ratios reflect the company’s solvency in the short term. Meeting current liabilities is related to business survival, while it is also helpful in raising additional capital on short notice.

In a stable economic environment, liquidity ratios are often ignored, but a small business must keep an eye on every liquidity ratio during a recession. Even during the 2008 housing bubble burst (recession), many strong companies with healthy assets on balance sheets defaulted due to failure to pay for daily operations, vendors, and short-term debt obligations.

Final Words

Financial metrics like liquidity ratios help to assess a company’s financial condition related to meeting its current debt obligations. A healthy liquidity ratio is a positive sign that its working capital management is efficient.

A company should hold enough cash to cushion against any emergency. At the same time, carrying too much cash shows a mismanagement of resources that could have been invested. The level of cash a company should hold differs with the industry type.

An accounting software like Akounto helps you track your finances like a pro. Akounto’s intuitive dashboard allows you to track your income and expenses and monitor your growth toward projected profits. Visit Akounto’s website to know more!