What is Trial Balance in Accounting?

A trial balance lists the closing balances of all accounts of the general ledger at the end of the accounting period. The balances in the trial balance are mentioned as credit or debit balances.

[ez-toc]

A trial balance is the first step in the building blocks of making financial statements.

Trial balances have debit and credit columns and list account balances of all general ledgers at the end of an accounting period.

In double-entry bookkeeping, all the debit balances should be equal to all the credit balances when all the account balances in the trial balance are totaled. In case there is a mismatch, it represents or hints towards errors in bookkeeping.

Trial balances are not all comprehensive tools for detecting bookkeeping and accounting errors. There are certain types of errors that trial balances can detect, and then there are a whole lot of errors which does not impact trial balance totals and thus go undetected. Do you know bookkeeping and accounting are different?

Purpose of Trial Balance in Accounting Systems

The trial balance in an accounting system serves as a diagnostic tool, ensuring the mathematical accuracy of the double-entry accounting system and also ensures that each entry is posted twice following the basic rule of the accounting equation.

Recording financial transactions in bookkeeping starts with posting journal entries to their respective general ledger accounts. In many cases, even journal entries are skipped, and direct ledger account postings are made.

Every account in the general ledger can have only one entry, multiple entries, or no entry at all for the accounting period under question. For example, inventory, revenue, sales, cash, and bank are likely to have multiple entries. In contrast, fixed assets can have a few or one entry in certain cases, retained earnings can have no impact in an accounting period, and the balance is carried forward to the next accounting cycle.

Keeping all this in mind, the ending balance of all the ledger accounts is taken in a trial balance and added to check for certain kinds of errors. The thumb rule is that all the credit and debit balances should tally; a mismatch represents underlying errors in recording transactions.

The trial balances lay the foundation for preparing financial statements, as they verify the accuracy of the transaction recording systems and ensure that the financial position is represented truly and reliably.

With the use of accounting software, the trial balance is automatically generated, and the arithmetical accuracy of the accounting data can be checked anytime with just a few clicks.

Trial Balance Example

The following table presents the trial balance format:

|

Accurate Accounting Knowledge Providers Inc. |

|||

|

Account Number |

Account Name |

Account Balance |

|

| В | В |

Debit ($) |

Credit ($) |

|

XX-XXX-XXX |

Cash in Hand |

XXXX |

В |

|

XX-XXX-XXX |

Petty Cash |

XXXX |

В |

|

XX-XXX-XXX |

Bank |

XXXX |

В |

|

XX-XXX-XXX |

XXXX |

В | |

|

XX-XXX-XXX |

Inventory |

XXXX |

В |

|

XX-XXX-XXX |

Debtors |

XXXX |

В |

|

XX-XXX-XXX |

Prepaid Expenses |

XXXX |

В |

|

XX-XXX-XXX |

Property, Plant and Equipment |

XXXX |

В |

|

XX-XXX-XXX |

XXXX |

В | |

|

XX-XXX-XXX |

Selling Expenses |

XXXX |

В |

|

XX-XXX-XXX |

XXXX |

В | |

|

XX-XXX-XXX |

Income Tax Expense |

XXXX |

В |

|

XX-XXX-XXX |

Rent |

XXXX |

В |

|

XX-XXX-XXX |

Salaries |

XXXX |

В |

|

XX-XXX-XXX |

Common Stock |

В |

XXXX |

|

XX-XXX-XXX |

В |

XXXX |

|

|

XX-XXX-XXX |

Additional Paid-in Capital |

В |

XXXX |

|

XX-XXX-XXX |

Treasury Stock |

В |

XXXX |

|

XX-XXX-XXX |

В |

XXXX |

|

|

XX-XXX-XXX |

В |

XXXX |

|

|

XX-XXX-XXX |

Deferred Revenue |

В |

XXXX |

|

XX-XXX-XXX |

В |

XXXX |

|

|

XX-XXX-XXX |

Sales |

В |

XXXX |

|

XX-XXX-XXX |

Purchase Return |

В |

XXXX |

|

XX-XXX-XXX |

Long Term Debt |

В |

XXXX |

|

TOTAL |

XXXX |

XXXX |

|

Types of Trial Balances

There are 3 types of Trial Balance:

- Unadjusted Trial Balance

- Adjusted Trial Balance

- Post-closing Trial Balance

1. The unadjusted trial balance

The unadjusted trial balance refers to a trial balance before making any rectification or adjustment entries. It is the initial trial balance report where the accrued or deferred adjustments are still not made.

The unadjusted trial balance can be called an initial draft to check the integrity of general ledger accounts made to date. However, the basic rule of all the debit and credit balances to match holds true to check any possible errors.

2. The adjusted trial balance

An adjusted trial balance is made after adjusting entries into the general ledger accounts, which may include accrued, estimated, or deferred amounts. It is prepared to present a fair picture of the financial position before closing or finalizing all the ledger accounts.

3. The post-closing trial balance

A post-closing trial balance contains the permanent accounts where the closing balances or entries are passed, and other (revenue, expense, dividend, etc.) accounts are adjusted to the retained earnings. The post-closing trial balance contains only permanent accounts

Methods to Prepare a Trial Balance in Accounting

Totals Method

The totals method to prepare a trial balance includes calculating all the debits and credit entries of all the ledger accounts separately and then posting them on the debit and credit columns of the trial balance.

Balances Method

In the balances methods to prepare trial balances, the ending balances of all the individual accounts are taken and then added to the trial balance to check if the debit and credit balances match and if there is integrity in the accounting system or if it has errors.

Totals-cum-Balances Method

Total-cum-balances method to prepare trial balances includes totaling the debit and credit balances of every account and listing them along with their account balances. This method aims to ensure integrity both at the micro level of accounts and the macro level of accounting systems so that accurate data is used to generate financial statements.

8 Types of Errors Highlighted by Trial Balance

- Mathematical errors

- Transposition errors

- Posting errors

- Wrong account entries

- Incorrect account balance

- Reversal errors

- Recording errors

- Extraction errors

1. Mathematical Errors

Explanation: Mistakes made during arithmetical calculations like adding, subtracting, etc.

Example: The accountant adds up the debits and gets a total of $5,000 instead of the correct $4,500.

2. Transposition Errors

Explanation: When two digits are reversed.

Example: Recording an amount as $54 instead of $45 in the general ledger.

3. Posting Errors

Explanation: Errors were made while transferring journal entries to ledger accounts.

Example: Posting a debit entry as a credit or vice versa.

4. Wrong Account Entries

Explanation: Recording transactions in incorrect accounts.

Example: Crediting the “Accounts Receivable” instead of “Accounts Payable” for payment received.

5. Incorrect Account Balance \ Casting Error

Explanation: Miscalculating the final balance of an account.

Example: If the ending balance of an account is $200 but is mistakenly recorded as $2,000 in the trial balance.

6. Reversal Errors

Explanation: When debit and credit entries are reversed.

Example: Debiting the “Cash” account and crediting the “Sales” account for a sale, instead of the other way around.

7. Recording Errors

Explanation: Not recording a transaction or recording it more than once.

Example: Forgetting to record a bank transaction or recording a single purchase twice.

8. Extraction Errors

Explanation: The balances from the ledger were wrongly entered in the trial balance.

Example: The asset account has the closing balance of $230,948 as a debit balance; while copying into the trial balance, either it was wrongly posted to the credit side or entered under some other item.

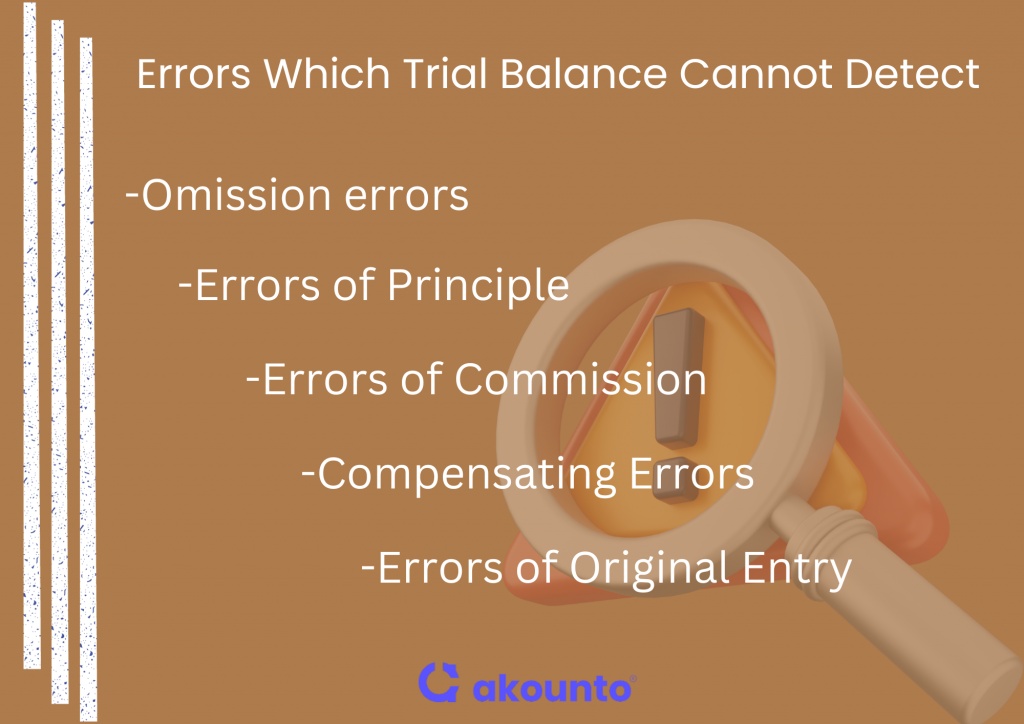

5 Errors Which Trial Balance Cannot Detect

- Omission errors

- Errors of Principle

- Errors of Commission

- Compensating Errors

- Errors of Original Entry

1. Omission Errors

Explanation: Transactions are completely omitted from the books.

Example: A sale made to a customer is neither debited to “Accounts Receivable” nor credited to “Sales.”

2. Errors of Principle

Explanation: A transaction that’s recorded against the fundamental principles of accounting.

Example: Capital expenditure, like purchasing machinery, is recorded as a revenue expenditure in the “Repairs and Maintenance” account.

3. Errors of Commission

Explanation: Mistakes made in the process of recording a transaction.

Example: Writing the wrong amount in the ledger or posting the amount in the account of a similar-named customer.

4. Compensating Errors

Explanation: Two or more errors that nullify the effect of each other.

Example: Under-debiting one account by $100 and over-debiting another account by the same amount.

5. Errors of Original Entry

Explanation: Recording the wrong initial amount before posting.

Example: Recording a purchase of $450 as $540 in the purchase journal.

Conclusion

Trial balance is a crucial cog in the preparation of financial statements. It verifies the accuracy of entries in the general ledger by simply ensuring that debits equal credits. It detects basic errors that impact trial balance totals and sets the stage for the next process, which is the preparation of final accounts.

Visit Akounto’s blog to learn more about the topics of accounts and finance that help you run a small business efficiently and effectively.